Table of Contents

- Overview & Purpose: Ethics IAR CE Policy Brief for IARs

- Ethics IAR CE Framing: Why This Matters for Investment Advisers

- NASAA’s Role in Investor Protection and Market Oversight

- The CLARITY Act in Regulatory Context

- Core Ethics Issue: Inconsistent Asset Definitions and Fiduciary Clarity

- Ethical Implications for Advisers and Clients

- Core Ethics Issue No. 2: Preserving the Investment-Contract Framework

- Ethical Significance of Enforcement Flexibility

- Core Ethics Issue No. 3: Federal Preemption and State Antifraud Authority

- The Ethical Role of State Regulators in Fraud Prevention

- NASAA’s Requested Legislative Adjustments

- What Advisers Should Take From This CLARITY Act Analysis for IAR Ethics CE

- Conclusion: Ethics, Judgment, and Regulatory Change

- Annotated Letter: NASAA Expresses Concerns Regarding the Digital Asset Market Clarity Act

- Annotated Letter: NASAA Expresses Concerns Regarding the Digital Asset Market Clarity Act

- FAQs

Overview & Purpose: Ethics IAR CE Policy Brief for IARs

This CLARITY Act Analysis for IAR Ethics CE summarizes and explains the January 13, 2026 letter issued by the North American Securities Administrators Association (NASAA) to the leadership of the U.S. Senate Committee on Banking, Housing, and Urban Affairs regarding the Digital Asset Market Clarity Act (the “CLARITY Act”). It is written for Registered Investment Advisers and Investment Adviser Representatives (IARs) seeking knowledge of the regulatory context, substance of NASAA’s concerns with CLARITY, and the potential implications for investor protection. This is an ethics issue for all advisers and it is knowledge integrated with A4A CLARITY Act Analysis For IAR Ethics CE.

This post is informational and explanatory. It does not take a position on the merits of the CLARITY Act legislation, does not assess compliance obligations, and does not provide legal advice. Instead, this CLARITY Act Analysis for IAR Ethics CE explains how state securities regulators view the current draft of the bill and why those views matter to advisers whose professional responsibilities are grounded in fiduciary duty and client-first behavior, and how you can receive NASAA ethics IAR CE on this subject in live and on-demand classes. All descriptions reflect NASAA’s stated positions as expressed in its letter.

Ethics IAR CE Framing: Why This Matters for Investment Advisers

For investment advisers, the issues raised in NASAA’s letter go well beyond statutory drafting or agency jurisdiction. They speak directly to fiduciary judgment and professional ethics. Advisers operate at the intersection of investor protection, market innovation, and client trust, and must regularly decide whose interests their conduct aligns with when regulatory frameworks are contested or unsettled.

The CLARITY Act debate, as framed by NASAA, presents a stark policy choice: whether regulatory change prioritizes consumer protection and fraud deterrence, or emphasizes regulatory relief and certainty for digital asset providers. For fiduciaries, this distinction matters. Brokers are generally accountable to their broker-dealers’ supervisory structures, while fiduciaries are obligated to act in the best interests of clients. This CLARITY Act Analysis for IAR Ethics CE brings that tension into plain view. It does not argue a side, but it removes filters and abstractions, allowing advisers to see—clearly—how competing regulatory approaches may affect enforcement capacity, investor outcomes, and the ethical posture of the advisory profession itself.

NASAA’s Role in Investor Protection and Market Oversight

NASAA is the association representing state, provincial, and territorial securities and commodities regulators across the United States, Canada, and Mexico. In the U.S., NASAA members are the primary enforcers of state securities laws and play a central role in licensing RIA firms and professionals, examining registrants, investigating misconduct, and enforcing antifraud provisions.

Since the passage of the National Securities Markets Improvement Act of 1996 (NSMIA), state and federal regulators have operated under a cooperative federalism framework designed to divide responsibility rather than duplicate it. Under this framework, Congress preempted states from requiring their own registration of securities that are offered nationally, assigning that function to federal regulators to promote efficiency and uniformity. At the same time, states retained core investor-protection authority, including licensing and oversight of firms and professionals, investigative powers, and antifraud enforcement.

NASAA evaluates the CLARITY Act against this long-standing allocation of authority and argues that the bill risks disturbing that balance. From an ethics perspective, the concern is not institutional turf, but whether changes in regulatory structure could reduce the speed or effectiveness of fraud response—outcomes that directly affect clients.

The CLARITY Act in Regulatory Context

The CLARITY Act is a legislative effort to establish a comprehensive federal framework for regulating digital assets, including cryptocurrencies and blockchain-based tokens. Its stated purpose is to reduce regulatory uncertainty by clarifying asset classifications, allocating jurisdiction between federal regulators, and creating a more predictable environment for innovation.

NASAA acknowledges these objectives and explicitly states that it supports responsible innovation in financial markets. The association also notes that it previously engaged with congressional staff on earlier drafts of the legislation and that some revisions reflect that input. Despite those changes, NASAA concludes that the current version of the CLARITY Act—particularly Title I—raises unresolved concerns that could weaken investor protection if enacted without further amendment. On March 3, 2026, in a L:IVE IAR CE class, you can hear an informed perspective at financial consumer advocate Michael Canning's session providing CLARITY Act Analysis for IAR Ethics CE.

Core Ethics Issue: Inconsistent Asset Definitions and Fiduciary Clarity

A central concern raised by NASAA is that the CLARITY Act introduces new digital-asset classifications that are both unfamiliar and difficult to reconcile with long-standing securities law concepts. To understand NASAA’s objection, it helps to start with how the bill attempts to sort digital assets into regulatory categories before assigning oversight authority.

The CLARITY Act introduces the concept of a “network token,” which it treats as a type of digital commodity rather than a security for purposes of federal securities law. In general terms, a digital commodity is intended to resemble assets whose value derives from use within a system rather than from a legal claim on a business or issuer. Under the bill, a network token is described as being intrinsically linked to a distributed ledger or blockchain network and valued primarily for its function or use within that network.

The bill then creates a related but distinct category called an “ancillary asset.” Ancillary assets are defined as a subset of network tokens whose value depends on the entrepreneurial or managerial efforts of an identifiable originator or related party. NASAA emphasizes that reliance on the efforts of others is a defining characteristic of an investment contract under existing securities law.

At the same time, the CLARITY Act excludes from network-token status any digital asset that provides traditional financial rights, such as profit-sharing, dividends, liquidation rights, or equity-like interests. NASAA argues that this creates a structural contradiction: an asset may depend on managerial or entrepreneurial efforts to generate value, yet be legally prohibited from conveying the types of financial rights that typically arise from those efforts. This is included in A4A CLARITY Act Analysis For IAR Ethics CE classes.

From an ethical and professional standpoint, this definitional structure matters because advisers rely on coherent regulatory concepts to evaluate products, assess risk, and explain protections to clients. When legal classifications diverge from economic reality, advisers may find it more difficult to communicate where investor protections begin and end. NASAA’s concern is not merely technical; it reflects the risk that novel labels such as “network token” or “digital commodity” could obscure meaningful differences in risk, accountability, and enforceability that fiduciaries are ethically obligated to consider. If you want to diver deeper, former policy director for NASAA, Michael Canning on March 3 speaks live and provides incisive CLARITY Act Analysis for IAR Ethics CE.

Ethical Implications for Advisers and Clients

Ambiguous definitions can create space for regulatory arbitrage, where products are structured to avoid oversight while still being marketed with profit expectations. For advisers, this raises ethics-driven questions about due diligence, client communication, and reliance on regulatory labels that may not align with underlying risk.

Advisers are not regulators, but they are expected to exercise independent judgment in the best interests of clients. A framework that weakens clarity around when investor protections apply may increase the ethical burden on advisers to compensate for regulatory gaps through enhanced scrutiny, clearer disclosure, and more conservative client guidance.

Core Ethics Issue No. 2: Preserving the Investment-Contract Framework

NASAA places particular emphasis on preserving the existing legal concept of an investment contract, which has long served as a flexible, fact-based tool for determining when an arrangement should be treated as a security. At the center of that concept is the idea that an investor is relying on the entrepreneurial or managerial efforts of others to generate a return.

This reliance matters because it identifies situations where investors are vulnerable to information asymmetry and promotional abuse. When value depends on someone else’s managerial skill, judgment, or continued involvement, investors cannot independently protect themselves through use or control of the asset. Securities law has historically stepped in at that point to require disclosure, impose antifraud obligations, and provide regulators with enforcement authority.

NASAA explains that many digital asset scams do not resemble traditional securities offerings. Instead, they often involve unlicensed promoters, informal marketing through social media, secondary-market trading, and evolving narratives about future utility or network growth. In these cases, the investment-contract framework allows regulators to look past labels and technical design to assess economic reality—specifically, whether purchasers are relying on others’ efforts for profit.

The CLARITY Act does not expressly eliminate the investment-contract doctrine. NASAA does not claim that it does. However, NASAA warns that provisions directing or empowering the SEC to narrow how “entrepreneurial or managerial efforts” are defined or applied could make it easier for promoters to design products that technically fall outside the narrowed framework while preserving economic dependence on their efforts. CLARITY Act Analysis For IAR Ethics CE on A4A with Michael Canning is expected to address these ethics issues for IARs

Ethical Significance of Enforcement Flexibility

CLARITY Act Analysis for IAR Ethics CE is not about whether innovation should occur, but whether enforcement tools remain effective. Advisers serve clients who may be exposed—directly or indirectly—to digital asset markets. Weakening enforcement frameworks may increase the likelihood that clients encounter fraudulent or misleading products before regulators can intervene.

NASAA’s position highlights an ethical tension advisers must navigate: supporting innovation while remaining alert to how regulatory changes may reduce investor protections. Ethical practice requires advisers to consider not just what is permitted under law, but how changes in enforcement capacity may affect client outcomes.

Core Ethics Issue No. 3: Federal Preemption and State Antifraud Authority

Another major focus of NASAA’s letter is federal preemption. NASAA acknowledges that Congress has made revisions to better preserve state authority, including removing language that could have limited state licensing and registration powers for firms and professionals.

However, NASAA argues that the CLARITY Act still risks expanding federal preemption beyond the limits established by NSMIA. In particular, NASAA is concerned that certain provisions could be interpreted to preempt state antifraud authority in digital asset transactions, including secondary-market activity.

NASAA emphasizes that NSMIA deliberately preserved state antifraud enforcement even where federal law preempts registration requirements. From NASAA’s perspective, maintaining this balance is essential to investor protection and to the ethical functioning of the regulatory system advisers rely on.

The Ethical Role of State Regulators in Fraud Prevention

NASAA underscores that state regulators are often the first to detect and pursue digital asset fraud, particularly in cases involving local victims or smaller-scale schemes. The association notes that digital asset fraud disproportionately affects older investors.

For advisers, this reinforces the ethical importance of robust enforcement systems. State antifraud authority functions as a backstop that supports client trust in financial markets. Weakening that authority may shift more risk onto investors and, indirectly, onto advisers tasked with guiding them. MIchael Canning's LIVE March 3, 2026 class delivers CLARITY Act Analysis for IAR Ethics CE

NASAA’s Requested Legislative Adjustments

NASAA does not call for abandonment of federal digital asset legislation. Instead, it proposes targeted revisions, including aligning definitions of network tokens and ancillary assets, explicitly preserving state antifraud authority consistent with NSMIA, limiting SEC rulemaking authority that could narrow investment-contract principles, and adding robust antifraud savings clauses throughout Title I.

NASAA frames these changes as necessary to maintain regulatory balance, protect investors, and provide durable clarity that does not fluctuate with political transitions.

What Advisers Should Take From This CLARITY Act Analysis for IAR Ethics CE

This CLARITY Act Analysis for IAR Ethics CE from Mike Canning of LXR Group, a Washington DC consulting firm, is expected not expected to say this signals immediate regulatory change. Instead, Canning, who has a history of working for organization seeking to protect financial consumers, is expected to say it clarifies how state regulators assess pending legislation and the ethical principles that inform their position.

For advisers, key takeaways include how regulatory structure influences investor protection outcomes, whether clarity achieved through preemption may come at the cost of enforcement effectiveness, and how fiduciary judgment applies when regulatory policy choices favor market efficiency over consumer safeguards.

Conclusion: Ethics, Judgment, and Regulatory Change

NASAA’s January 2026 letter presents a clear, unfiltered view of how state securities regulators evaluate the CLARITY Act. While supporting modernization of digital asset regulation, NASAA urges Congress to avoid weakening antifraud enforcement and foundational investor-protection principles.

For investment advisers, the significance of this debate lies not in statutory mechanics, but in ethical judgment. Advisers must operate within evolving regulatory environments while maintaining a client-first posture. CLARITY Act Analysis for IAR Ethics CE provides the factual context necessary for advisers to understand the stakes, assess competing policy approaches, and reflect on how regulatory design intersects with fiduciary responsibility.

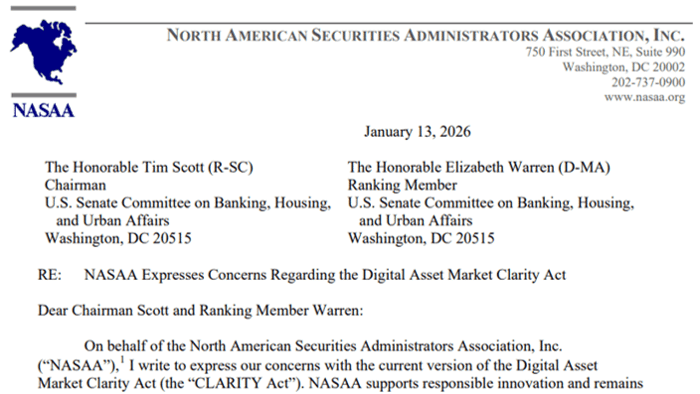

Annotated Letter: NASAA Expresses Concerns Regarding the Digital Asset Market Clarity Act

This is the letter sent by NASAA on Jan. 13, 2026 to Senate Banking Committee expressing concerns about the Digital Asset Market Clarity Act. Highlighted words contain insights, sources, and links for additional information. Hover (desktop) or tap (mobile) to see analysis and links. Annotations do not represent the views of NASAA and are intended solely to educate IARs.

NORTH AMERICAN SECURITIES ADMINISTRATORS ASSOCIATION, INC.

January 13, 2026

RE: Digital Asset Market Clarity Act

NASAA supports responsible innovation and remains committed to working constructively with Congress to develop an effective regulatory framework for digital assets that preserves state authority under NSMIA.

However, NASAA is unable to support the CLARITY Act in its current form because Title I would weaken state authority to combat fraud and abuse in digital asset transactions.

I. Asset Definitions

The CLARITY Act contains internal inconsistencies that undermine regulatory clarity.

The separation of managerial effort from meaningful financial rights departs from traditional economic logic.

Investment contract analysis remains the primary tool regulators use to combat digital asset fraud.

Fraudsters will exploit limits, often harming older investors.

II. Preemption

Congress should narrow preemption to preserve state antifraud authority.

The Act grants expansive discretion to the SEC, risking policy instability.

NASAA urges a robust antifraud savings clause and warns against narrowing investment contracts.

NASAA stands ready to work with Congress to ensure that any legislation strikes a balanced, clear, and effective approach to digital asset regulation that protects investors, preserves state authority, and promotes responsible innovation.

Should you or your colleagues have any questions, please do not hesitate to contact NASAA or its policy staff.

Sincerely,

Marni Rock Gibson

NASAA President

CC: Members of the U.S. Senate

FAQs

Why did NASAA oppose the CLARITY Act?

NASAA opposed the CLARITY Act as drafted because it concluded that certain provisions could weaken state securities regulators’ ability to protect investors from fraud and abuse, particularly in digital asset markets. NASAA’s concerns focus on definitional inconsistencies, expanded federal preemption, and potential limits on long-standing antifraud tools rather than opposition to digital asset innovation itself.

What does “nixed” mean in the context of NASAA’s CLARITY Act letter?

“Nixed” is a shorthand way of describing NASAA’s refusal to support the CLARITY Act in its current form. NASAA did not reject federal digital asset legislation outright. Instead, it stated that the bill requires material changes before it could be supported, particularly to preserve state antifraud authority and established investor-protection frameworks.

How does the CLARITY Act affect state securities regulators?

The CLARITY Act could affect state securities regulators by expanding federal preemption beyond the balance established under NSMIA. NASAA warns that, if preemption is broadened or made unclear, states may lose the ability to investigate and prosecute digital asset fraud—especially in secondary-market transactions where scams frequently occur.

What is NSMIA and why does it matter in this debate?

The National Securities Markets Improvement Act of 1996 (NSMIA) created a cooperative federalism framework that preempted certain state registration requirements while explicitly preserving state antifraud enforcement. NASAA uses NSMIA as the benchmark for evaluating the CLARITY Act, arguing that the bill risks upsetting that long-standing balance between federal efficiency and state-level investor protection.

What are “network tokens” and why is NASAA concerned about their definition?

Under the CLARITY Act, “network tokens” are treated as digital commodities rather than securities. NASAA is concerned that the bill’s definition allows tokens to depend on managerial or entrepreneurial efforts while excluding traditional financial rights, creating categories that may be difficult to enforce and easy for bad actors to exploit.

What does “entrepreneurial or managerial efforts” mean in securities law?

“Entrepreneurial or managerial efforts” refers to situations where investors rely on the ongoing work, decisions, or expertise of others to generate profits. This concept is central to the investment-contract framework and helps regulators identify when securities-law protections should apply because investors cannot protect themselves through control or use of the asset.

Why is NASAA focused on preserving the investment-contract framework?

NASAA views the investment-contract framework as the primary and most flexible tool regulators use to combat evolving digital asset scams. Because fraud schemes change quickly, a principles-based approach allows regulators to focus on economic reality rather than technical labels. NASAA warns that narrowing this framework could reduce consumer protection.

How is this an Ethics IAR CE issue rather than just a regulatory dispute?

This issue raises ethics and fiduciary questions because advisers must decide how to evaluate products, explain risks, and protect clients in unsettled regulatory environments. If regulatory changes weaken enforcement tools or create ambiguous protections, advisers may bear greater responsibility to compensate through heightened due diligence and client communication.

Does NASAA oppose digital asset innovation?

No. NASAA explicitly states that it supports responsible innovation in financial markets. Its objections to the CLARITY Act relate to investor protection and enforcement capacity, not opposition to blockchain technology or digital assets themselves.

What should investment advisers take away from NASAA’s CLARITY Act letter?

Advisers should understand how regulatory structure affects investor protection, recognize that legal labels may not always reflect economic risk, and apply fiduciary judgment when regulatory frameworks are in flux. NASAA’s letter highlights why advisers cannot rely solely on classification or compliance labels when acting in clients’ best interests.

How does this analysis relate to IAR Ethics CE requirements?

Ethics IAR CE focuses on fiduciary duty, client-first behavior, professional judgment, and navigating regulatory gaps. NASAA’s CLARITY Act letter provides a real-world case study in how regulatory design, enforcement authority, and investor harm intersect—making it directly relevant to ethics and professional responsibility education for IARs.