Table of Contents

- A Confluence of Concerns

- Retail Distribution, Accredited Investor Reform, and Systemic Risk

- Why Fiduciaries and Regulators Are Structurally Aligned

- U.S. Private Market Expansion Into Retail Channels

- Accredited Investor Changes and Retail Exposure

- Federal–State Friction and Fiduciary Alignment

- Why Private Market Risks for IARs Require Vigilance

- FAQs

Private market risks for IARs have changed considerably in recent years. No longer peripheral to portfolio construction, the risks of private investments in this moment are more important to portfolio management decisions.

Over the past decade, and especially since 2020, private credit, interval funds, and other retail-accessible private vehicles have expanded at a pace that materially alters the investment landscape for U.S. advisers and their clients. This article contains evidence for IARs to consider about whether private deal risk may be posing new risks to investors that fiduciaries are obliged to protect clients from. This is not merely asset-class growth. It reflects a structural shift in how capital is raised, valued, distributed, and regulated.

Private markets were historically institutional domains. Pension funds, endowments, and sovereign investors bore the illiquidity, leverage, valuation opacity, and complexity risks inherent in private equity and direct lending. Retail investors largely accessed diversified, liquid public markets governed by standardized disclosure and daily price discovery. That balance is changing — and fiduciary obligations need to evolve with it.

A Confluence of Concerns

Capital is flowing into crypto ventures, AI-driven enterprises, and alternative private investments at a pace that continues to reshape the capital formation landscape. Much of that growth is occurring outside the public markets, through Regulation D offerings, private funds, and other exempt transactions. At the same time, the regulatory environment is evolving.

Recent Supreme Court decisions have affected certain SEC administrative enforcement procedures — particularly how the agency conducts in-house proceedings — but they have not eliminated the SEC’s statutory enforcement authority. Executive branch priorities can also influence enforcement focus and rulemaking direction, yet they do not remove powers granted by Congress.

Meanwhile, policy debates are intensifying around federal preemption from state regulation. Industry groups have advocated for harmonized national frameworks in areas such as crypto, AI, and digital financial services, arguing that a patchwork of state regulation creates friction and uncertainty. State regulators and investor advocates have pushed back, emphasizing local oversight and investor protection.

Overlaying all of this is a renewed push to broaden the accredited investor definition. That effort is coming from multiple directions:

• The SEC expanded the definition in 2020 to include certain professional credentials, moving beyond pure income and net-worth thresholds.

• Members of Congress have introduced legislation — including the Equal Opportunity for All Investors Act and related proposals — that would further expand eligibility through exams or certification pathways.

• Advocacy organizations and industry participants continue to press for additional access reforms, often framing them as capital formation and investor choice initiatives.

Taken together, these developments raise a structural question:

As private market access expands and eligibility standards potentially widen, what guardrails should accompany that expansion?

The debate is not simply about access. It is about alignment — between capital formation, enforcement architecture, and investor protection in an increasingly complex market ecosystem.

The direction of travel is clear: private capital is growing, eligibility standards are under review, and regulatory authority is being tested and recalibrated. How these forces converge will shape the next phase of U.S. financial regulation.

Retail Distribution, Accredited Investor Reform, and Systemic Risk

Retail channels increasingly include interval funds, non-traded vehicles, evergreen private credit structures, and other registered products designed to hold illiquid assets. Assets in these vehicles have grown sharply in recent years. At the same time, regulatory changes and legislative proposals have broadened the accredited investor definition, expanding eligibility beyond traditional income and net worth thresholds to include certain credential-based pathways — and potentially further reforms.

In plain English, accredited investor reform allows more individuals to invest in private, illiquid, and less transparent securities that were previously restricted. While expanded access may be framed as democratization, it also shifts greater private-market exposure onto households that may lack institutional liquidity buffers.

This convergence increases private market risks for IARs in several ways:

Liquidity risk becomes more difficult to model, especially in stress cycles

Appraisal-based valuations can mask volatility until redemption pressure emerges

Credit-cycle sensitivity may not be evident during expansionary periods

Fee layering and leverage structures can amplify downside risk

The macroeconomic implications are not trivial. As capital migrates from public markets into private structures, price discovery shifts from continuous market-based valuation to periodic appraisal methodologies. During stable markets, this may appear benign. During downturns, however, liquidity constraints and valuation lag can expose fragilities simultaneously across funds.

If accredited investor standards continue to broaden while retail distribution accelerates, the private market becomes increasingly intertwined with household balance sheets. What was once institutional risk becomes retail exposure. That does not automatically imply systemic instability, but it does increase the probability that stress events transmit more directly to individual investors.

Private investments are not inherently inappropriate. They may provide diversification and income benefits. But they operate under different transparency and liquidity dynamics than public securities. Redemption windows replace daily trading. Disclosure standards vary. Valuations rely on models rather than market clearing prices. These structural differences change the risk profile — particularly when access expands.

Why Fiduciaries and Regulators Are Structurally Aligned

Tension between regulators and industry has existed throughout modern history. What distinguishes this period is the combination of rapid retailization of private markets and the expansion of investor eligibility standards.

For state-registered IARs operating under a fiduciary standard, this debate is not abstract policy friction. It affects client liquidity planning, valuation transparency, portfolio concentration limits, documentation standards, and professional liability exposure.

When NASAA raises concerns about expanding retail access to opaque private assets without corresponding disclosure safeguards, that position happens to overlap with an IAR's fiduciary obligations. Both fiduciaries and state regulators share an interest in ensuring that access expansion does not outpace investor protection. And IARs will experience heightened liability risk and, thus, higher liability insurance premiums.

Understanding private market risks for IARs is not about resisting innovation. It is about recognizing structural changes in U.S. capital markets and evaluating whether investor protection mechanisms are evolving at the same pace as distribution.

U.S. Private Market Expansion Into Retail Channels

Private markets in the United States have grown substantially over the past twenty years. Historically, private equity and private credit were institutional domains — pensions, endowments, sovereign funds. Today, retail distribution vehicles have accelerated access.

Interval Funds: A Retail Access Proxy

Interval funds are registered under the Investment Company Act of 1940 but provide limited liquidity. They have become one of the clearest U.S. “wrapper” structures for private strategies.

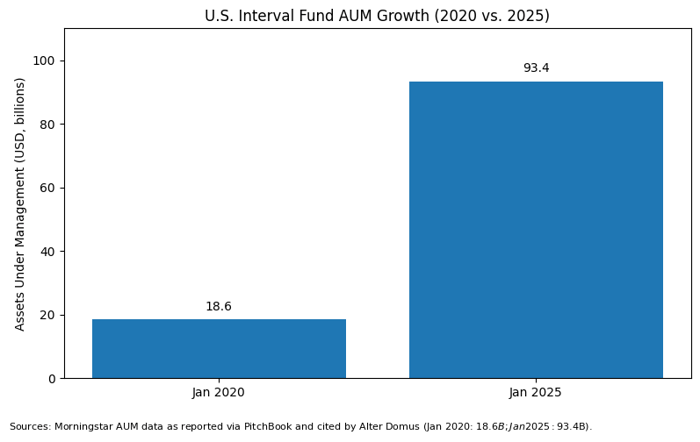

U.S. Interval Fund Assets

| Year | Approximate AUM |

|---|---|

| January 2020 | ~$18.6 billion |

| 2023 | ~$90+ billion |

| January 2025 | ~$93.4 billion |

That represents roughly fivefold growth in five years.

For fiduciaries, rapid expansion in retail-accessible private vehicles increases the need for:

Liquidity stress testing

Disclosure clarity

Valuation methodology review

Client suitability reassessment

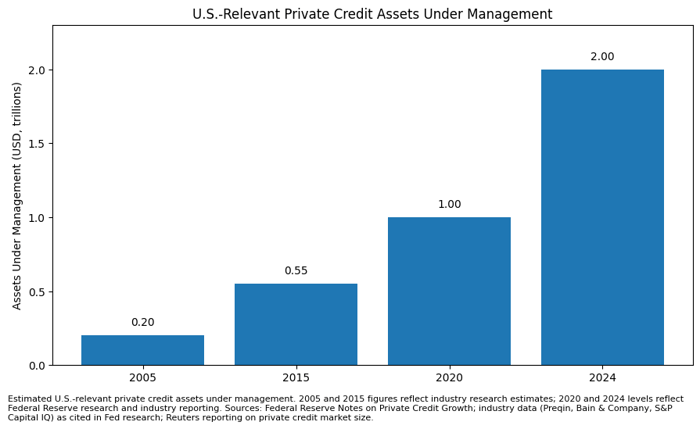

U.S. Private Credit Growth

Private credit is now a multi-trillion-dollar U.S. market.

Estimated U.S.-Relevant Private Credit AUM

| Year | Approximate AUM |

|---|---|

| 2005 | <$200 billion |

| 2015 | ~$500–600 billion |

| 2020 | ~$1 trillion |

| 2024 | ~$2 trillion+ |

Federal Reserve research and ratings agency commentary have noted both scale and increasing retail exposure.

Private market risks for IARs increase when illiquid assets are distributed more broadly without equivalent transparency enhancements.

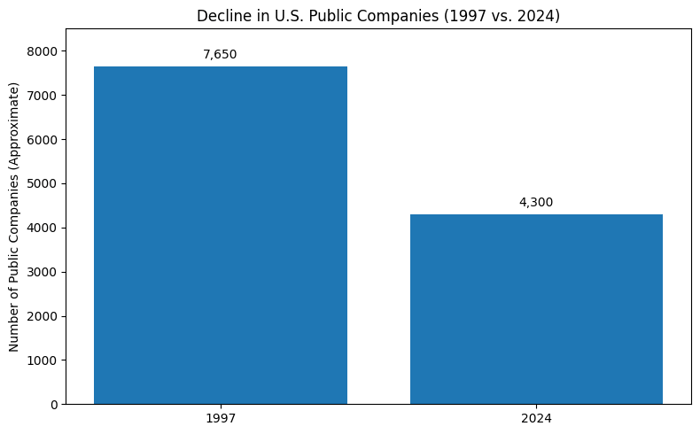

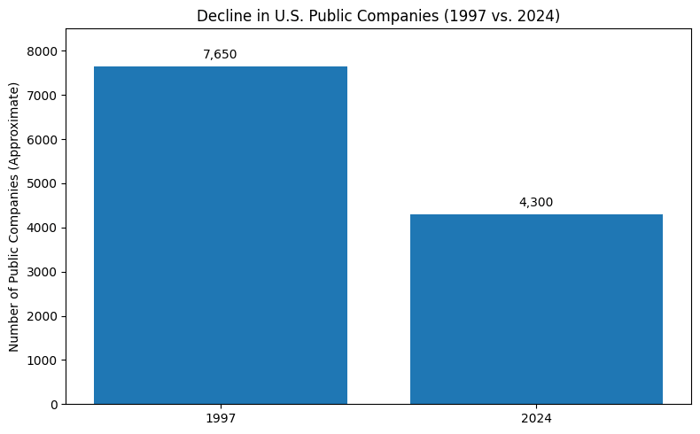

Shrinking Public Market Universe

While private investment assets have experience huge growth, the number of publicly traded U.S. companies has declined materially since the late 1990s. With companies able to access capital from private sources, the relative attractiveness of going public is diminished. The change in capital formation has altered the risk of the U.S. economy.

investments in private markets are not subject to the same scrutiny as public company investments. When you buy a share in a publicly held company, you know it's subject to annual audits by independent accounting firms, quarterly SEC reporting requirements and you know what your investment would be worth if you chose to sell it today. None of that is necessarily true of private market investments. This raises private market risks for IARs

| Year | Approximate Public Companies |

|---|---|

| 1997 | ~6,500–8,800 |

| 2024 | ~3,900–4,700 |

As more corporate growth occurs in private markets, advisers face greater pressure to incorporate private allocations — even when liquidity and valuation standards differ significantly from public markets.

As more corporate growth occurs in private markets, advisers face greater pressure to incorporate private allocations — even when liquidity and valuation standards differ significantly from public markets.

Accredited Investor Changes and Retail Exposure

Private market risks for IARs are magnified when eligibility standards evolve.

Historically, accredited investor qualification relied primarily on:

$200,000 annual income ($300,000 joint), or

$1 million net worth excluding primary residence

Recent changes expanded eligibility to certain credential holders. Legislative discussions have considered further expansion.

In plain English: more individuals could qualify to invest in private, illiquid offerings previously limited to higher wealth thresholds.

Why This Matters to Fiduciaries

Private investments often:

Lack daily liquidity

Use appraisal-based valuations

Provide limited standardized disclosure

Include layered management and performance fees

If eligibility expands without parallel disclosure reform, retail investors may gain access without gaining transparency.

For fiduciaries, this creates:

Increased due diligence burden

More complex liquidity alignment decisions

Greater behavioral risk in opaque pricing environments

Heightened conflict management obligations

Private market risks for IARs therefore include not only investment risk, but regulatory and professional risk.

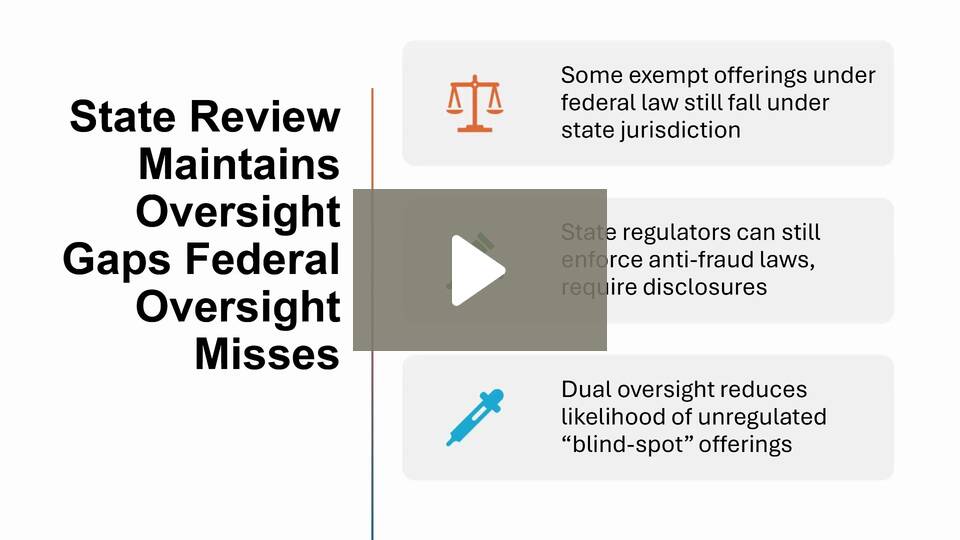

Federal–State Friction and Fiduciary Alignment

Tension between federal regulators and state regulators is not new. However, current debates involve:

Retail access to private markets

Federal preemption of state authority

Digital asset oversight

AI-enabled investment platforms

State regulators, acting through NASAA, emphasize:

Retail investor protection

Guardrails before eligibility expansion

Preservation of enforcement authority

Industry coalitions representing segments of private equity sponsors, private credit managers, and alternative investment platforms frequently advocate streamlined compliance and broader access.

For state-regulated IARs, private market risks are not abstract. If eligibility expands while enforcement authority narrows, fiduciaries may face greater client exposure with fewer regulatory backstops.

Fiduciary duty requires:

Acting in the client’s best interest

Providing full and fair disclosure

Managing liquidity appropriately

Mitigating conflicts

When regulators call for transparency before expansion, that position aligns structurally with fiduciary obligations.

Why Private Market Risks for IARs Require Vigilance

Private markets are not inherently unsuitable. They may provide diversification, income, and access to growth sectors unavailable in public markets.

But structural shifts matter.

Rapid retailization of private credit and interval funds, combined with potential accredited investor expansion, increases:

Liquidity mismatch risk

Valuation opacity

Fee complexity

Regulatory exposure

For IAR fiduciaries, professional vigilance is not optional. It is embedded in the duty of care.

Understanding private market risks for IARs is therefore part of responsible advisory practice in 2026 and beyond.

Advisors4advisors is going to be offering classes focusing on this important investor protection topic. One class class is about a move to preempt NASAA from regulating private investments, crypto, alternatives and AI based investments, which I teach. It is available on demand and a live class will be conducted on February 25, 2026. A sample of the class is below.

The other class related to the push to weaken state regulation of private investments will be taught by Mike Canning, former public policy director and chief spokesman for NASAA who has more recently served as a policy consultant to organizations including Consumer Federation and AARP. That will be a March 3 update on IAR Regulation.

FAQs

What are private market risks for IARs?

Private market risks for IARs include liquidity constraints, valuation opacity, leverage exposure, layered fee structures, and limited standardized disclosure. Because private investments often rely on appraisal-based pricing and periodic redemption windows, IARs must ensure clients understand and can tolerate these structural risks.

Why are private market risks increasing for retail investors?

Private market risks are increasing as retail access expands through interval funds and private credit vehicles, and as accredited investor standards broaden. More individuals now qualify to invest in private offerings, which may expose portfolios to illiquidity and valuation uncertainty not present in public securities markets.

How does private credit growth affect IAR fiduciary duty?

Private credit growth increases responsibility because credit-cycle risk, leverage exposure, and liquidity limits may amplify downside outcomes during economic stress. IARs must stress-test portfolios and clearly disclose how private credit differs from publicly traded fixed income.

What ethical considerations arise when recommending private investments?

Ethical considerations include full and fair disclosure, liquidity alignment, fee transparency, and conflict mitigation. IARs must avoid presenting private investments as equivalent to publicly traded securities and must clearly explain redemption limitations and valuation methodologies.

What changes to the accredited investor definition raise concerns?

Recent expansions to the accredited investor definition allow more individuals to qualify based on credentials rather than traditional wealth thresholds. Legal eligibility does not eliminate the duty of care. IARs must evaluate suitability independently of investor qualification status.

Why are regulators concerned about expanding retail access to private markets?

Regulators emphasize that private offerings typically provide less standardized disclosure and limited liquidity. If eligibility expands without corresponding safeguards, retail investors may assume risks they do not fully understand — increasing investor-protection concerns.

How are IARs and state regulators aligned on private market risks?

Both emphasize investor protection, transparency, and suitability analysis. When regulators advocate caution before expanding retail access to opaque assets, that position reinforces IAR obligations to act in clients’ best interests.

What macroeconomic risks accompany private market expansion?

As more capital migrates into private structures, price discovery shifts from daily market pricing to periodic appraisals. During downturns, liquidity mismatches and valuation lag may expose fragilities. Increased retail participation can amplify household exposure to these risks.

How should IARs document private market recommendations?

IARs should document liquidity analysis, client risk tolerance, fee disclosures, redemption mechanics, and stress assumptions. Clear documentation supports fiduciary compliance and regulatory expectations.

Does this topic qualify for Ethics IAR CE?

Yes. Private market risk analysis implicates fiduciary duty, disclosure obligations, conflict mitigation, and client-first decision-making. Education examining liquidity constraints, valuation transparency, and suitability considerations may support Ethics IAR CE classification under NASAA standards.

What factors are converging to elevate private market risks?

Several developments are occurring simultaneously: rapid growth in private credit and interval funds, expanded retail distribution channels, broader accredited investor eligibility, and shifting regulatory authority debates. Together, these factors increase exposure to illiquid, valuation-based investments at the same time investor access is widening.

Why does the convergence of these factors increase risk to consumers?

When retail access expands while liquidity constraints and appraisal-based valuations remain unchanged, consumers may face risks they do not fully understand. During stable markets, these risks may appear muted. In downturns, redemption limits, credit losses, and valuation adjustments can become more pronounced.

How does accredited investor reform interact with private market growth?

Accredited investor reform increases the number of individuals legally eligible to invest in private offerings. When eligibility expansion coincides with rising private credit distribution, more households may gain exposure to complex structures. Legal qualification does not eliminate liquidity, leverage, or transparency risks.

What is the risk to financial advisers as private markets retailize?

As private market distribution expands, advisers assume greater responsibility for explaining structural differences between public and private assets. Failure to adequately disclose liquidity constraints, valuation methodologies, or fee layering may increase regulatory scrutiny and professional liability exposure.

Why can private market risks appear lower than they are?

Private assets are often valued periodically rather than through continuous market pricing. This can produce smoother reported returns in stable environments. However, appraisal-based valuation does not eliminate underlying credit or liquidity risk. During stress periods, adjustments may occur more abruptly.

How could economic downturns amplify private market risks?

In downturns, private credit defaults may rise, leverage may magnify losses, and redemption requests may increase simultaneously. Limited liquidity structures can delay exits, exposing investors to prolonged recovery periods. Retail participation increases the potential impact on household balance sheets.

Does increased retail access automatically mean systemic instability?

Not necessarily. However, when private market growth, expanded eligibility standards, and retail distribution acceleration occur together, household exposure to less liquid assets increases. The interaction of these factors can heighten vulnerability during credit contractions.

Why is the convergence of retail expansion, accredited investor reform, and private credit growth a topic of ethics IAR CE?

The convergence of retail expansion, accredited investor reform, and private credit growth directly implicates fiduciary duty, disclosure obligations, and client-first decision-making. Evaluating whether access expansion outpaces transparency safeguards is central to ethical advisory practice.