Table of Contents

- Ethics IAR CE Questions Financial Advisers Are Asking

- Patchwork Securities Regulatory System and the New Ethics for Fiduciaries, a Topic of an Ethics IAR CE Class

- Federal Preemption and Investor Protection

- Crypto Valuation and Fiduciary Duty

- Venture Exchanges and the Expansion of Private Markets

- Regulation A+, Crowdfunding, and the Liquidity Problem

- Venture Capital Incentives and Insider Information Advantages

- State Regulators Seek a Limited Role in Crypto Oversight

- Why Regulators Do Not View the CFP Board as a Government Authority

- Financial Regulation News For IARs Quarterly

- FAQs

Financial regulation is in one of the most consequential periods of change in modern U.S. history. Congressional proposals affecting cryptocurrency, artificial intelligence, and private securities markets could reshape how fiduciary advisers operate in important ways. Keeping up with these developments is central to understanding how crypto regulation affects fiduciary duties by imposing duties of care, loyalty, disclosure, and client protection to crypto investments, which are not regulated the same way as securities.

Michael J. Canning brings a rare perspective to financial regulatory debates—one shaped by deep experience in policymaking. Before founding the Washington policy consulting firm, LXRDC, in 2020, Canning spent a decade as regulatory policy chief at the North American Securities Administrators Association (NASAA), the organization representing state securities regulators in the United States. Prior to that, he worked for nearly a decade on Capitol Hill in legislative staff positions connected to the House Financial Services Committee during the drafting of major financial legislation following the 2008 financial crisis. He has experience in writing federal investor protection legislation.

For the past five years, he has worked as a lobbyist and consultant for Consumer Federation of America, AARP, and other groups focused on protecting financial consumers. More recently he has consulted on financial regulation to Free Trade Zones in South Asia.

The combination of regulatory, legislative, and policy advocacy experience allows him to describe the historic shift now underway in U.S, financial regulation. Developments in financial and technological innovation—cryptocurrency, artificial intelligence, and expanding private capital markets—are reshaping

Crypto regulation affects fiduciary duties and expands IAR ethical risks by adding a new set of ethical obligations for fiduciaries, which is why it is the subject of a 2026 ethics IAR CE class.

As a reporter who has covered financial regulation and capital markets since 1983, I am thrilled to use my conversation with Mike Canning to provide IAR CE through dialogue rather than a traditional lecture. The interview format prompts explanations revealing how regulatory policy gets formulated—how legislation moves through Congress, regulators interpret statutes, and how industry lobbying influences financial rules.

Some of the most important quotes from the 54-minute interview with Canning are below in italics and followed by context and analysis.

Ethics IAR CE Questions Financial Advisers Are Asking |

What are the new ethics for fiduciaries in financial advice? |

Crypto regulation affects fiduciary duties and is likely to expand IAR ethical risks and fiduciary responsibilities, which must evolve as financial regulation changes. Congressional proposals affecting crypto assets, private markets, and artificial intelligence appear to be poised to reshape investor protections and disclosure standards. Fiduciary advisers must understand how these developments alter due-diligence expectations and client communication responsibilities. |

How crypto regulation affects fiduciary duties? How crypto regulation affects fiduciary duties? |

Financial regulation defines the environment in which fiduciaries operate. When laws governing digital assets, private securities, or federal preemption change, the risks faced by retail investors change as well. now that crypto regulation is likely to expand IAR ethical risks, advisers must adapt their due-diligence practices and disclosures accordingly. |

How could federal preemption affect investor protection? |

Federal preemption can shift regulatory authority from state securities regulators to federal agencies. While this may simplify regulatory frameworks, it can also reduce local enforcement against fraud affecting retail investors. Fiduciary advisers must understand how these changes influence investor protections and adjust their oversight and disclosure practices accordingly. |

Why are private markets and crypto raising new fiduciary ethics questions? |

Private securities markets and cryptocurrencies lack the transparency and disclosure requirements of securities investments in public companies. The information gaps create new challenges for fiduciary advisers evaluating investment suitability and risk of a new, untested investment with none of the public accounting, reporting, and market rules governing shareholders and bond investors. As crypto instruments and their variants as well as other private investment market exchanges expand, advisers must reassess how they fulfill duties of prudence, care, and disclosure because crypto regulation affects fiduciary duties directly. |

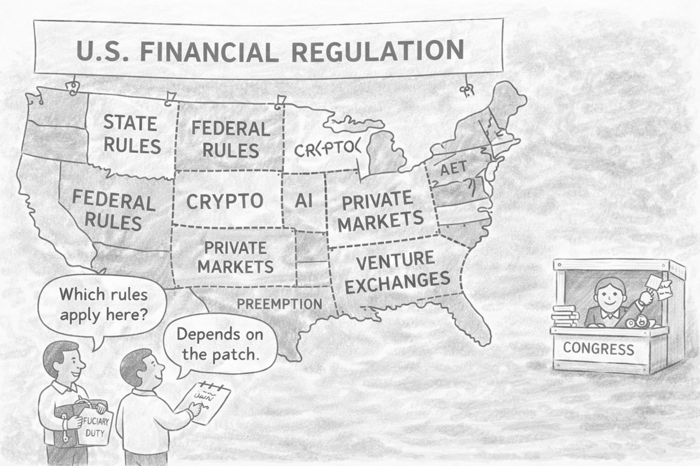

Patchwork Securities Regulatory System and the New Ethics for Fiduciaries, a Topic of an Ethics IAR CE Class

"I've spent my entire career working…for, with, or around…financial regulators, and I've never met a more dedicated group of regulators than the state securities regulators."

In explaining the U.S. system of state financial regulation, Mike Canning describes state securities oversight as “a slow, cumbersome, patchwork of a regulatory framework.” Inherent inefficiency keeps the state regulatory effort free of politics.

State governments frequently operate under structural budget constraints—such as balanced-budget requirements, cyclical tax revenues, and rising mandatory spending—that can leave public agencies chronically underfunded or facing periodic fiscal shortfalls during economic downturns. Only the most dedicated professionals civil servants thrive and rise to the top.

NASAA operates with only about thirty employees while coordinating regulatory policy across U.S. states, Canadian provinces, and Mexican jurisdictions. Much of the policy work therefore relies on regulators themselves rather than centralized staff.

Only about thirty-five states actively participate in NASAA initiatives. Many state securities chiefs are experienced attorneys who could earn far more in the private sector but remain in government roles for decades.

State securities laws evolved independently over decades, producing a regulatory landscape where authority is shared between state agencies and federal regulators but implemented through different statutes, enforcement priorities, and resources.

Understanding this fragmented structure is central to fulfilling the new ethical obligations of fiduciaries.

From Canning's description, because state regulatory powers are fragmented, with state financial laws differing from one state to another, state securities regulators have little political will or power. As a result, the professionals drawn to public service in state securities departments tend to be extremely dedicated. For every opening to serve on a NASAA committee developing regulatory policy, Canning says, three or four volunteers must be turned away,

While critics sometimes frame the system as inefficient, the decentralized structure allows local regulators to pursue fraud cases and investor complaints federal agencies lack resources to properly address.

Federal Preemption and Investor Protection

"It has potentially catastrophic…implications for mom and pop investors if preemption is done…recklessly or overly broadly.''

Federal preemption of state securities regulation is the most consequential Congressional debate affecting financial advisers today.

Preemption can simplify regulation and reduce compliance costs, but it may also remove the local enforcement authority that state regulators use to pursue smaller fraud cases affecting retail investors. Federal preemption of state regulatory authority is proposed as a way to support innovation and democratize capital formation.

For fiduciaries advising individual clients, this shift raises an ethical question: who protects investors if regulatory authority becomes concentrated at the federal level?

Advisers may need to compensate for reduced regulatory oversight through stronger due diligence and clearer client disclosures. These developments illustrate how crypto regulation affects fiduciary duties. Fewer than a quarter of all U.S> IARs always act as fiduciaries in advising clients. Nearly 80% of IARs are affiliated with a broker-dealer and licensed to sell securities and can switch hats from fiduciary to securities sales anytime.

Crypto Valuation and Fiduciary Duty

"What's the intrinsic value of, like, Bit Dollar or Doge Dogecoin. There is none…it's an instrument that trades purely on hype."

Canning's crypto critique reflects the perspective of former SEC Chair Gary Gensler and other policymakers who say cryptocurrencies possess no intrinsic fundamental economic value.

Traditional securities derive value from earnings, assets, or contractual cash flows. Many cryptocurrencies lack those anchors.

For fiduciaries, the ethical challenge involves determining whether recommending such assets meets standards of prudence, suitability, and informed consent. The debate over speculative assets increasingly seems likely to redraw ethics boundaries for fiduciaries when fiduciary advice hinges on evaluating investments that may have limited fundamental valuation frameworks and no history of market trading, much less a record of stability through crises.

Venture Exchanges and the Expansion of Private Markets

"What they're talking about in respect to a venture exchange…private securities would trade there…without quarterly disclosures or earnings calls."

Congressional proposals could allow exchanges that trade private securities while benefiting from federal preemption of state regulation.

Public companies must meet strict disclosure standards.

Private securities often do not.

If venture exchanges expand, fiduciary advisers could face markets where reliable financial information is limited.

This environment may redefine the new ethics for fiduciaries, a topic of an ethics IAR CE class, because advisers must determine how to evaluate investments lacking the transparency expected in public markets.

Point is, crypto regulation affects fiduciary duties and seems likely to expand IAR ethical risks and rewrite the obligations of investing in a new speculative asset class, which can be justified as a way of diversifying beyond securities. This is likely to be a fraud magnet for shady operators.

Regulation A+, Crowdfunding, and the Liquidity Problem

"Regulation A+ securities and crowdfunding expanded access to private investments but still lack secondary markets and liquidity."

The JOBS Act in 2012 attempted to expand investment access by allowing retail investors to participate in smaller capital-raising offerings, Canning says. However, these securities frequently lack active trading markets, analyst coverage, and consistent disclosures.

Without liquidity or reliable valuation data, investors may struggle to exit positions or determine fair market value, Canning warns. For fiduciary advisers, these challenges reinforce the new ethics obligations for fiduciaries. Expanded investment access increases the responsibility to explain complex risks to more investors and is occurring as the definition of an accredited investor is expected to be expanded.

Venture Capital Incentives and Insider Information Advantages

"For every Facebook there are ten thousand startups that fail…venture investors know first."

Venture capital firms often obtain privileged information through board seats and early funding roles. Retail investors typically lack access to that information.

If private securities markets expand, insiders at private companies may use new exchanges to exit positions before negative developments become public. Without the structural guardrails and investor protections in securities these investments will present a new set of risk considerations for investors and alter ethics considerations for fiduciaries.

Recognizing these structural incentives is likely to revamp how crypto regulation affects fiduciary duties become part of the new ethics obligations of fiduciaries, who will need to evaluate whether private investment opportunities primarily benefit insiders rather than clients.

The same way crypto regulation affects fiduciary duties, private investments are likely to be popularized and impose new responsibilities on fiduciaries to explain how their risk characteristics are entirely different from securities.

State Regulators Seek a Limited Role in Crypto Oversight

"States want a NSMIA-like framework…giving up licensing but keeping enforcement authority."

Under emerging legislative proposals, states may relinquish licensing authority for crypto issuers but retain enforcement authority to protect investors from fraud. While mentioning that state regulators are expected to retain their enforcement powers over crypto, Canning says their powers may be federally preempted in other ways. This compromise is being carved out in crypto legislative proposals make their way through Congress now.

Maintaining meaningful enforcement while allowing innovation is increasingly the direction of regulators, which is why crypto regulation is likely to expand IAR ethical risks.

Advisers must think ahead and anticipate the changes to operate responsibly in markets where regulatory authority is evolving.

Why Regulators Do Not View the CFP Board as a Government Authority

"State regulators view the CFP Board as a private accrediting organization rather than a regulator."

While it seemed far afield from how crypto regulation affects fiduciary duties the issue of the CFP Board's role in the regulatory framework was brought up by Canning. He touched on an issue that's dogged the CFP Board since it separated from the College of Financial Planning nearly four decades ago and established itself as an independent not for profit organization dedicated to establishing practice standards and regulating use of the CFP mark.

To be clear, the CFP Board sets professional standards and ethics requirements for financial planners but does not possess government enforcement authority. Like all individuals and companies,

Canning says regulators are irked by CFP Board portraying itself as a government regulator when it is not empowered by state or federal law. CFP Board can sue a CFP for bad behavior, but it cannot shut down a bad operator or throw them in jail.

In contrast, CPA regulation is empowered under state law. Every state has an independent Board of Accountancy responsible for licensing requirements imposed on CPAs. The boards are usually nominated by governors and appointed by the state senate.

We were out of time and did not get to question Mike about this comment, but I will next time.

Financial Regulation News For IARs Quarterly

At the end end of the session, Mike Canning threatens to teach on A4A again and I'd be honored to share his observations as financial regulatory legislation moves toward enactment in 2026. A4A will provide at least one class each quarter about the news on crypto regulation and private venture investment trade exchanges, which Canning discussed.

We've covered IAR CE about crypto previously, and Canning gives fiduciaries an insider's perspective on a regulatory shift underway now that will fundamentally change a fiduciary's obligations and increase a professional's liability. Crypto regulation affects fiduciary duties, and other changes in private investments are in the works that also will change the shape of IAR duties of care.

There are about 400,000 state and federally registered IARs in the U.S, and only 85,184 are not affiliated with a broker dealer, which means they are always fiduciaries. If you are in that group, advisors4advisors is an authoritative source for ethics IAR CE about financial regulation news affecting fiduciaries, and is tracking how crypto regulation affects fiduciary duties.

FAQs

What are the new ethics for fiduciaries in financial advice?

The new ethics for fiduciaries, a topic of an ethics IAR CE class, refers to how fiduciary responsibilities evolve as financial regulation changes. Legislative proposals affecting cryptocurrency, private markets, and artificial intelligence may reshape investor protections and disclosure requirements. Fiduciary advisers must understand how these changes influence due diligence, suitability analysis, and client communication.

Why do regulatory changes matter for fiduciary advisers?

Financial regulation defines the framework within which fiduciaries operate. When laws governing crypto assets, private securities markets, or federal preemption of state oversight change, the risks faced by retail investors change as well. Advisers must adapt their research, disclosure, and suitability practices to reflect the evolving regulatory environment.

How could federal preemption affect retail investors?

Federal preemption can shift regulatory authority from state securities regulators to federal agencies. While this may simplify regulatory frameworks, it can reduce the ability of local regulators to pursue smaller fraud cases affecting retail investors. Fiduciary advisers must understand how these changes influence the protections available to their clients.

Why are private securities markets raising fiduciary ethics questions?

Private securities often lack the transparency, research coverage, and reporting requirements that exist in public markets. As proposals emerge to expand secondary trading in private securities, fiduciary advisers must carefully evaluate whether these investments provide adequate information and liquidity for retail clients.

What risks do venture exchanges pose for retail investors?

Venture exchanges could allow certain private securities to trade publicly while benefiting from federal preemption of state regulation. However, these securities may lack quarterly disclosures, analyst coverage, or consistent financial reporting. Fiduciary advisers must assess whether these investments can be evaluated prudently on behalf of clients.

Why do insiders often have advantages in private investment markets?

Venture capital investors frequently hold board seats and have early access to company information. This gives insiders insights into a company’s prospects before information becomes available to public investors. Fiduciary advisers must understand how these informational advantages can affect investment risk for retail clients.

How does cryptocurrency raise ethical questions for fiduciary advisers?

Many cryptocurrencies lack traditional valuation anchors such as earnings, dividends, or assets. Because prices may depend largely on speculation or market sentiment, fiduciary advisers must determine whether clients fully understand the risks associated with recommending such investments.

Why do state securities regulators matter for investor protection?

State regulators often investigate smaller fraud cases affecting retail investors that federal agencies may lack resources to pursue. They also oversee investment advisers registered at the state level. Changes to federal preemption could therefore alter the enforcement landscape that protects ordinary investors.

How does political influence affect financial regulation?

Financial legislation is often shaped by lobbying, campaign financing, and political incentives. Industry groups may advocate for regulatory frameworks that support innovation or capital formation. Fiduciary advisers must understand the policy environment shaping investment markets so they can evaluate risks affecting clients.

Why do regulators distinguish between professional credentials and regulatory authority?

Professional organizations such as the CFP Board establish ethical standards and certification requirements. However, enforcement authority for financial regulation typically resides with government agencies. Fiduciary advisers must understand the distinction between professional standards and regulatory oversight.

What should fiduciaries learn from regulatory debates about crypto and private markets?

Fiduciaries should recognize that emerging financial technologies and new capital-raising structures may introduce risks that differ from traditional securities markets. Ethical financial advice requires understanding both the regulatory environment and the structural incentives affecting investment products.

Why is this discussion relevant for ethics IAR CE?

Ethics IAR CE focuses on the professional responsibilities of fiduciary advisers when serving clients. Regulatory developments affecting digital assets, private markets, and federal preemption directly influence how advisers evaluate risks, communicate with clients, and fulfill fiduciary duties.