Table of Contents

- 4-Minutes from Crypto Investing Risks CE

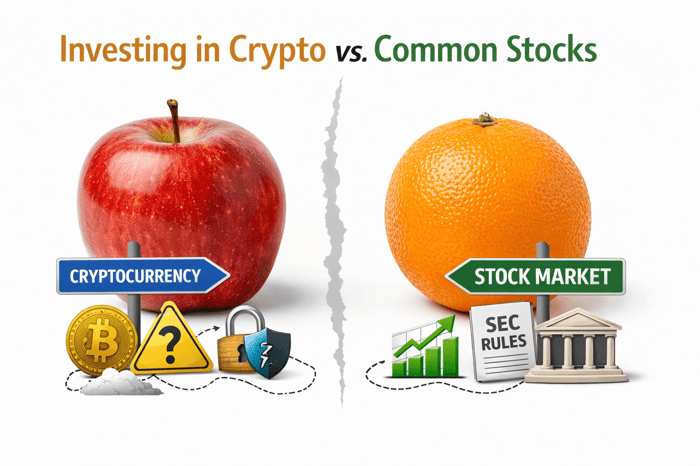

- Crypto Risks Versus Protections Taken For Granted

- Innovation or Regulatory Arbitrage?

- Crypto Risks for Fiduciaries in Tokenized Securities

- Lessons From Regulatory Gaps

- Crypto Risks for Fiduciaries and Stablecoin Representations

- Jurisdiction, Preemption, and Investor Protection

- Crypto Risks for Fiduciaries in Derivatives and Parallel Markets

- Communicating Complex Risk Clearly

- Integrating Crypto Risk Into Portfolio Construction

- Crypto Risks for Fiduciaries and the Moral Dimension

- Why This Is the Best 2026 IAR CE on Crypto Investing Risks

- Final Takeaway for Financial Professionals

- FAQs

Crypto risk for fiduciaries is in the news and this article serves as a clear warning. This class explains structural and ethical implications behind crypto products and its opposition to legislation regulating the industry. Crypto risk for fiduciaries is not just about volatility, price cycles, or speculation. It is about the integrity of market structure, regulatory protections for consumers, disclosure clarity, and the fiduciary obligations that govern CFP professionals, CPAs, CIMAs, and investment adviser representatives.

4-Minutes from Crypto Investing Risks CE |

When professionals search for the best 2026 IAR CE, they are looking for more than tax planning tips. They're looking for urgent and important news to their practice. That's why we have taken the step to proclaim Crypto Investing Risk For Fiduciaries one of the best IAR CE classes of 2026 in the title of this post. We only use this phrase to attract IARs for a good purpose: continuing education that addresses suitability, informed consent, systemic risk, and client communication in an environment where rules may not operate as they do in traditional securities markets. This article explains why crypto investing risks urgently require the attention of fiduciaries in 2026.

FAQs

Why is Crypto Risk For Fiduciaries different from general crypto volatility discussions?

Crypto Risk For Fiduciaries focuses on market structure, regulatory protections, and enforcement gaps—not just price swings. Fiduciaries must evaluate how structural differences affect disclosure, suitability, and informed consent.

Why is this considered one of the Best 2026 IAR CE classes?

It addresses urgent crypto regulatory developments affecting fiduciary liability and client protection. Advisers searching for the Best 2026 IAR CE need education that directly impacts practice risk.

What recent crypto regulatory news developments make this class urgent?

Legislative proposals involving tokenization, jurisdictional shifts, and potential state preemption may change investor protections. Crypto Risk For Fiduciaries explains how those developments could alter fiduciary responsibilities.

How does Crypto Risk For Fiduciaries apply to CFP® professionals?

CFPs are held to a fiduciary standard requiring full disclosure and informed consent. Structural differences in crypto regulation directly affect how CFP professionals evaluate suitability and explain risks.

Why should CPAs and CIMAs care about crypto regulatory structure?

CPAs and CIMAs advise on portfolio design, risk assessment, and due diligence. Crypto Risk For Fiduciaries highlights regulatory gaps that can materially affect portfolio integrity.

What does regulatory parity mean in crypto investing?

Regulatory parity means identical financial rights should receive identical oversight. The Best 2026 IAR CE emphasizes that clients often assume parity exists when it may not.

How does tokenization create Crypto Risk For Fiduciaries?

Tokenization may wrap traditional securities in a blockchain structure without identical oversight. Advisers must determine whether investor protections are equivalent.

Are stablecoins equivalent to bank deposits?

No. Stablecoins may not have equivalent capital requirements, examinations, or deposit insurance. Crypto Risk For Fiduciaries stresses the importance of explaining those differences clearly.

What is regulatory arbitrage and why does it matter to fiduciaries?

Regulatory arbitrage occurs when products are structured to avoid stricter oversight. Fiduciaries must identify when innovation reduces investor protections.

Could new crypto legislation reduce investor protections?

Certain proposals could shift jurisdiction or preempt state regulators. Crypto Risk For Fiduciaries explains how enforcement authority changes may limit client remedies.

How does Healthy Markets Association align with fiduciary interests?

Healthy Markets Association advocates for transparency, investor protection, and structural integrity—principles aligned with fiduciary obligations to act in clients’ best interests.

Why is Tyler Gellasch’s background relevant to advisers?

Tyler Gellasch worked on Dodd-Frank implementation and served at the SEC and in the U.S. Senate. His policy experience informs the structural warnings discussed in the Best 2026 IAR CE.

Is this class anti-crypto?

No. Crypto Risk For Fiduciaries does not condemn digital assets. It teaches advisers how to analyze structural risks ethically and defensibly.

How do regulatory gaps increase fiduciary exposure?

When oversight weakens, disclosure and due diligence burdens increase. Advisers may face greater liability if clients misunderstand structural protections.

Why is Crypto Risk For Fiduciaries more important in 2026 than before?

Regulatory debates over tokenization, stablecoins, and derivatives markets are accelerating. The Best 2026 IAR CE addresses developments affecting practice today.

How should advisers explain crypto custody risks?

Advisers should clarify who holds assets, how insolvency is handled, and what protections apply. Clear communication is central to Crypto Risk For Fiduciaries.

What is the ethical issue behind parallel markets?

Parallel markets may operate under different transparency standards. Fiduciaries must evaluate whether clients understand those differences.

Does this class address suitability analysis?

Yes. The Best 2026 IAR CE emphasizes that suitability requires understanding structural regulation, not just asset allocation.

Could crypto regulatory changes affect professional liability insurance?

Potentially. Increased fiduciary exposure due to structural risk may influence liability considerations, which Crypto Risk For Fiduciaries addresses.

Who should take this Best 2026 IAR CE class?

IARs, CFP® professionals, CPAs, and CIMAs who advise on investments and want to understand how crypto regulatory developments affect fiduciary duty and client protection.