Table of Contents

- Why financial planning for neurodivergent individuals is not a niche issue

- How many forms of neurodivergence are there?

- How Frank Murtha helped turn the idea into adviser education

- Financial planning for neurodivergent individuals starts with dignity and discovery

- Different clients need different safeguards

- Financial planning for neurodivergent individuals requires concrete communication

- Meetings should protect decision capacity

- Make implementation part of the recommendation

- How many forms of neurodivergence are there?

- FAQs

Financial planning for neurodivergent individuals is no longer a fringe topic. IA reps. CFP® professionals, CPAs, CIMAs, trust officers, and investment consultants already serve people who process information, uncertainty, emotion, social cues, math, time, organization, and follow-through differently. Some have formal diagnoses of autism, ADHD, dyslexia, OCD, anxiety, or related learning differences. Many do not. Others simply recognize small cognitive imperfections: they are terrible at spatial organization, struggle with basic calculations, freeze when instructions have too many steps, or need more time to translate numbers into real choices.

The point is not to diagnose. It is to make your professional advice usable. A financial plan can be technically sound and still fail if the client leaves confused, overloaded, embarrassed, or unable to complete the next step. The course also helps advisers feel more honest about their own limits. Everyone has some cognitive weakness, whether it involves math, memory, attention, spatial judgment, sensory tolerance, or turning complexity into action.

Why financial planning for neurodivergent individuals is not a niche issue

Some clients can build companies but cannot gather tax forms. Some understand markets but cannot tolerate fluorescent lights and rapid screen sharing. Some are brilliant specialists who need literal language, not metaphors. Some want to trade immediately when emotion spikes.

The work of financial planning for neurodivergent individuals belongs in mainstream practice because it helps diagnosed clients, undiagnosed clients, clients with “a touch” of autism, ADHD or other traits "on the spectrum," and clients who simply present this way under stress. Better communication helps all of them.

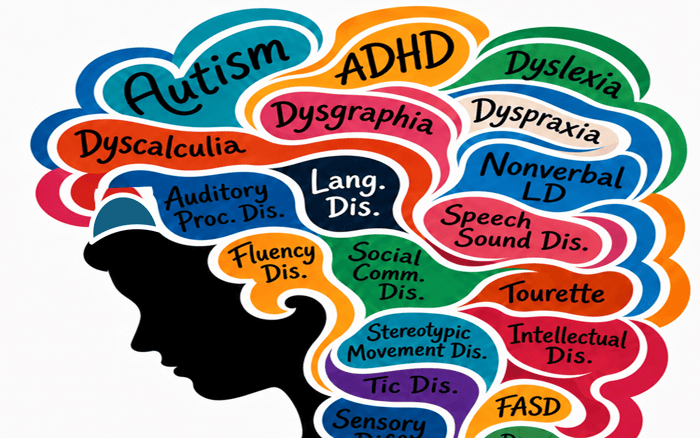

Neurodivergence is broader than autism and ADHD. The spectrum has no fixed number of forms, but advisers are likely to encounter clients with learning differences, communication differences, sensory processing differences, tic disorders, genetic developmental conditions, and other neurological or cognitive variations. Point is, we're living in an era where suddenly we've recognized that perhaps a third of the population is affected by neurodivergence and, as fiduciaries, you need to be prepared to your ethical best. In recognition of that need, two new Advisors4Advisors CE classes have recently been released. Here are links to the descriptions for the two classes:

Financial Advising Neurodivergence: Ethics IAR

Neurodivergence Advising In Practice

This is a proactive effort to help advisers searching for ethics CE about financial planning for neurodivergent individuals,

How many forms of neurodivergence are there?

There is no single official count of forms of neurodivergence. Autism and ADHD are two of the best-known examples, but the broader term is often used to describe many kinds of brain-based differences, including learning differences, communication differences, sensory processing differences, tic disorders, genetic developmental conditions, and other neurological or cognitive variations.

The table below is not a diagnostic checklist. It is a practical awareness tool for financial professionals. The advisory point is not to identify or label the client. The point is to recognize when communication, environment, pacing, documentation, or implementation needs to change so the client can understand the recommendation and act on it.

This working list includes 27 forms of neurodivergence commonly discussed and fiduciaries need to know about before providing financial planning for neurodivergent individuals.

| # | of neurodivergence | What it may affect | Why financial advisers may need to recognize it |

|---|---|---|---|

| 1 | Autism Spectrum Disorder | Social communication, sensory processing, routine, flexibility, focused interests | Clients may need direct language, predictable agendas, written summaries, and advance notice before change. |

| 2 | ADHD | Attention, impulse control, organization, time management, follow-through | Clients may benefit from shorter meetings, reminders, automation, and agreed-upon pauses before major decisions. |

| 3 | Dyslexia | Reading, decoding words, spelling, processing written language | Dense written plans, long disclosures, and document-heavy processes may be harder to absorb. |

| 4 | DyscalculiaForm | Numbers, math, quantities, calculations, numeric relationships | Percentages, tax estimates, investment returns, and budgeting may require simpler explanations and concrete examples. |

| 5 | Dysgraphia | Writing, spelling, handwriting, typing fluency, written expression | Forms, handwritten notes, signatures, and written responses may create friction |

See the full list of neurodivergent conditions at the bottom of this article.

How Frank Murtha helped turn the idea into adviser education

This article also grows out of a professional relationship that has turned into a friendship over the past five years. When I asked Frank Murtha, Ph.D., whether advisers needed a class on financial planning for neurodivergent individuals, he was immediately excited. He saw the gap: advisers are being asked to serve clients whose cognitive styles affect the planning process, yet few practical resources existed.

The idea for a class addressing financial planning for neurodivergent individuals came after I saw a class on the topic produced by NASAA members. It was a brilliant idea and I learned a lot by taking the NASAA course, but it goes into details IARs don't need to know. It was not directly applied to the financial advice process. The series of classes A4A about neurodivergence bridges that gap. Currently, these two classes are the only CE approved by NASAA dealing with financial planning for neurodivergent individuals.

Frank brought the intellectual framework, clinical insight, and teaching discipline. He also trusted us with his intellectual property, which made the collaboration more than a content project. It became a shared effort to translate psychology into adviser behavior: better questions, better pacing, better follow-up, and more dignity. That is the inspiring part. The work does not ask advisers to become therapists. It asks them to become more observant, more concrete, and more skillful in the way recommendations are delivered.

Financial planning for neurodivergent individuals starts with dignity and discovery

Start by asking clients how they prefer to communicate. Do they want an agenda in advance? Would a written summary help? Do they prefer email, secure messaging, phone, video, or in-person meetings? What causes financial tasks to stall? What kind of follow-up makes action easier?

These questions preserve dignity because they focus on process, not pathology. The adviser is not saying, “What is wrong with you?” The adviser is saying, “What conditions help you understand and act?”

This matters for financial planning for autistic individuals because predictability, low sensory load, direct language, and advance warning can reduce anxiety. It also matters for financial planning and ADHD because attention, time management, impulse control, and follow-through may be the practical risk points. The same client may need both support and autonomy: enough structure to act, but enough respect to remain fully in control.

Different clients need different safeguards

Autism and ADHD can create opposite planning risks. In financial planning for neurodivergent individuals, the practical question is whether the client needs a brake, a bridge, or both. A client with ADHD traits may seek novelty, interrupt, forget forms, abandon paperwork, or want to act on market stress immediately. A client with autism spectrum traits may need routine, resist abrupt change, interpret language literally, or become overloaded by ambiguity.

A brake slows action: a waiting period before trades, written confirmation before allocation changes, or a second review after a volatile market day. A bridge helps action happen: prefilled forms, checklists, direct upload links, staged implementation, scheduled reminders, and same-day recaps. Advisers should stop treating noncompletion as laziness or resistance. Often it is a process failure.

Financial planning for neurodivergent individuals requires concrete communication

Advisers often rely on language that feels professional but is vague: “reasonable risk,” “comfortable retirement,” “long term,” “appropriate allocation,” “soon,” or “enough income.” For some clients, those phrases create avoidable confusion. Concrete communication replaces generalities with numbers, dates, examples, ranges, and assigned responsibilities.

Instead of saying, “We need to know whether you will have enough income later,” say, “We are testing whether $8,500 per month after tax can last 30 years, assuming a 4% annual withdrawal and a separate reserve for health care.” Instead of “Please send the documents soon,” say, “Please upload the 2024 tax return and trust agreement by Friday at 3 p.m. using this link.”

In financial planning for neurodivergent individuals, concreteness is not simplistic. It is respectful. It reduces translation work and makes the client’s decision more observable.

Meetings should protect decision capacity

A meeting is not successful because the adviser covered every topic. It is successful when the client understands the decision and can act afterward. Use shorter meetings, clearer agendas, fewer decisions, and a recap at the end. Send the agenda in advance, but avoid rigid minute-by-minute time limits that may create pressure.

The environment also matters. Noise, bright light, alerts, cluttered screens, and rapid screen changes can consume attention. A quiet room, simple screen share, muted notifications, and deliberate pauses can improve judgment. In virtual meetings, show one document at a time and tell the client before switching topics.

Financial planning for neurodivergent individuals also requires a better understanding check. “Does that make sense?” often measures politeness, not comprehension. Try: “I want to make sure I explained that clearly. What do you understand the next step to be?” A client’s restatement gives the adviser evidence of understanding and reveals what needs clarification.

Make implementation part of the recommendation

A recommendation is incomplete until it can be executed by the client in front of you. Automate where appropriate: contributions, bill payments, transfers, rebalancing alerts, and recurring reviews. Automation can help clients with ADHD-related forgetfulness and support autistic clients who rely on routine. It should still be reviewed, explained, and controlled by the client.

The practical standard is consistent: ask communication preferences, keep meetings short, use literal language, share agendas, provide written follow-up, verify understanding, avoid taking style personally, automate, reduce sensory load, and create change safeguards. Use consistent labels and formats. Same-day recap. Clear action list. Deadlines. Ownership. One link. One request per paragraph.

For IA reps, CFPs, CPAs, CIMAs, CFAs, and other financial professionals, this is not soft work. It is risk management. It reduces misunderstanding, missed implementation, emotional decisions, and preventable client frustration. Financial planning for neurodivergent individuals sharpens the adviser’s core role: translating complexity into decisions a real person can understand, retain, and carry out.

The deeper lesson is humane. Every client has cognitive imperfections. Some are diagnosed. Some are not. Some simply need more clarity, more patience, or less noise. When advisers honor those differences, clients feel less ashamed and more capable, with a more reliable path from conversation to action in practice. That is better planning for neurodivergent clients, and it is better planning for everyone.

How many forms of neurodivergence are there?

There is no single official count of forms of neurodivergence. Autism and ADHD are two of the best-known examples, but the broader term is often used to describe many kinds of brain-based differences, including learning differences, communication differences, sensory processing differences, tic disorders, genetic developmental conditions, and other neurological or cognitive variations.

The table below is not a diagnostic checklist. It is a practical awareness tool for financial professionals. The advisory point is not to identify or label the client. The point is to recognize when communication, environment, pacing, documentation, or implementation needs to change so the client can understand the recommendation and act on it.

This working list includes 27 examples commonly discussed in connection with neurodivergence or neurodiversity.

| # | Form of neurodivergence | What it may affect | Why financial advisers may need to recognize it |

|---|---|---|---|

| 1 | Autism Spectrum Disorder | Social communication, sensory processing, routine, flexibility, focused interests | Clients may need direct language, predictable agendas, written summaries, and advance notice before change. |

| 2 | ADHD | Attention, impulse control, organization, time management, follow-through | Clients may benefit from shorter meetings, reminders, automation, and agreed-upon pauses before major decisions. |

| 3 | Dyslexia | Reading, decoding words, spelling, processing written language | Dense written plans, long disclosures, and document-heavy processes may be harder to absorb. |

| 4 | Dyscalculia | Numbers, math, quantities, calculations, numeric relationships | Percentages, tax estimates, investment returns, and budgeting may require simpler explanations and concrete examples. |

| 5 | Dysgraphia | Writing, spelling, handwriting, typing fluency, written expression | Forms, handwritten notes, signatures, and written responses may create friction. |

| 6 | Dyspraxia / Developmental Coordination Disorder | Coordination, motor planning, sequencing, physical organization | Paperwork, signatures, in-office tasks, or spatial organization may be harder than expected. |

| 7 | Nonverbal Learning Disorder / Developmental Visual-Spatial Disorder | Visual-spatial reasoning, patterns, social cues, mental imagery | This fits the client who cannot visualize how items fit in a trunk, closet, room, chart, or diagram. |

| 8 | Auditory Processing Disorder | Processing spoken information, especially in noisy settings | A client may hear the adviser but not accurately process everything said in a meeting. Written follow-up helps. |

| 9 | Language Disorder | Learning or using spoken, written, or signed language | Financial jargon, long explanations, and abstract language may reduce comprehension. |

| 10 | Speech Sound Disorder | Producing speech sounds clearly | Advisers should avoid interrupting, rushing, or misreading speech difficulty as lack of understanding. |

| 11 | Childhood-Onset Fluency Disorder / Stuttering | Speech flow, rhythm, timing, fluency | Give the client time to speak without completing sentences or moving too quickly. |

| 12 | Social Communication Disorder | Conversational rules, social cues, tone, context, pragmatic language | A client may miss implied meaning, sarcasm, or subtle cues. Direct communication is safer. |

| 13 | Tourette Syndrome | Motor and/or vocal tics | Tics should not be interpreted as disrespect, anxiety, impatience, or lack of attention. |

| 14 | Other Tic Disorders | Recurrent motor or vocal tics | Meetings may require patience, privacy, and a nonjudgmental tone. |

| 15 | Stereotypic Movement Disorder | Repetitive movements | Repetitive movement may be self-regulating, not a sign of disengagement. |

| 16 | Intellectual Disability / Intellectual Developmental Disorder | Cognitive and adaptive functioning beginning during development | Advice may need plain language, slower pacing, supported decision processes, and careful confirmation of understanding. |

| 17 | Sensory Processing Differences | Over- or under-responsiveness to sound, light, touch, texture, motion, smell, or other input | Bright lights, noisy offices, cluttered screens, or rapid screen sharing can impair decision quality. |

| 18 | Fetal Alcohol Spectrum Disorders | Learning, memory, behavior, judgment, impulse control, communication | Clients may struggle with memory, math, judgment, or follow-through. |

| 19 | Down Syndrome | Developmental and cognitive differences | Planning may require accessible communication and attention to long-term support needs. |

| 20 | DiGeorge Syndrome / 22q11.2 Deletion Syndrome | Development, learning, health, behavior | Advisers may need to coordinate financial planning with medical, family, benefit, and support considerations. |

| 21 | Prader-Willi Syndrome | Cognitive, behavioral, developmental, and appetite-regulation challenges | Planning may involve support structures, benefits coordination, and careful household financial design. |

| 22 | Williams Syndrome | Cognitive, social, and developmental traits | Clients may be highly social but still need clear explanation, safeguards, and support. |

| 23 | Fragile X Syndrome | Learning differences, developmental delays, autism- or ADHD-like traits | Advisers may encounter family planning, disability planning, benefits coordination, and supported decision-making issues. |

| 24 | Obsessive-Compulsive Disorder | Intrusive thoughts, compulsive behaviors, reassurance-seeking, control needs | Financial decisions may become stuck in checking, fear-based loops, or repeated requests for certainty. |

| 25 | Bipolar Disorder | Mood, energy, sleep, confidence, risk-taking, judgment | Advisers may need safeguards around major financial decisions during periods of elevated or depressed mood. |

| 26 | Social Anxiety Disorder | Social fear, meeting avoidance, discomfort with calls or performance situations | A client may avoid meetings, delay calls, appear overly agreeable, or say yes quickly to escape discomfort. |

| 27 | Developmental Prosopagnosia / Face Blindness | Recognizing faces | A client may fail to recognize an adviser or staff member. That should not be taken personally. |

The advisory point is not to identify or label the client. The point is to recognize when communication, environment, pacing, documentation, or implementation needs to change so the client can understand the recommendation and act on it. Moreover, knowing the long list of 27 forms of neurodivergence is a practical way to impart crucial information to provide financial planning for neurodivergent individuals

FAQs

What is financial planning for neurodivergent individuals?

Answer:

Financial planning for neurodivergent individuals is the process of adapting advice, meetings, communication, documentation, and follow-through so clients can understand recommendations and act on them. It does not require the adviser to diagnose autism, ADHD, dyslexia, dyscalculia, or any other condition. It requires the adviser to make the planning process clearer, calmer, more concrete, and easier to implement.

Question:

Why should financial advisers care about neurodivergence?

Answer:

Advisers already serve clients who process information, uncertainty, math, emotion, social cues, and follow-through differently. Some are diagnosed. Many are not. Others simply have cognitive quirks, such as difficulty with spatial reasoning, paperwork, numbers, sensory overload, or multistep instructions. Financial planning for neurodivergent individuals helps advisers make advice usable for real people, not imaginary perfect decision-makers.

Question:

Does financial planning for neurodivergent individuals mean diagnosing clients?

Answer:

No. Advisers should not diagnose, treat, or label clients. The adviser’s role is to observe what helps the client understand, decide, and act. That may mean asking about communication preferences, using clearer language, reducing sensory distractions, shortening meetings, confirming understanding, or providing written next steps.

Question:

How is financial planning for autistic individuals different?

Answer:

Financial planning for autistic individuals often benefits from predictability, direct language, low-stimulation meetings, advance notice before changes, and written summaries. Some autistic clients may prefer more time to process information, fewer surprises, and clear explanations of what will happen next. The goal is not to stereotype the client, but to create a process that respects how the client best receives and uses information.

Question:

How does financial planning and ADHD affect adviser-client meetings?

Answer:

Financial planning and ADHD often requires attention to follow-through, paperwork, time management, distraction, impulse control, and emotional reactions to market stress. A client with ADHD traits may benefit from shorter meetings, fewer open loops, reminders, automation, direct upload links, and agreed-upon waiting periods before major investment changes.

Question:

Why is concrete language so important in financial planning for neurodivergent individuals?

Answer:

Vague phrases such as “reasonable risk,” “comfortable retirement,” “long term,” or “send this soon” can create confusion. Concrete language uses numbers, dates, examples, deadlines, and clear ownership. For example, “upload the 2024 tax return by Friday at 3 p.m.” is more useful than “send the tax documents soon.” Concrete language reduces avoidable misunderstanding.

Question:

What meeting adjustments help neurodivergent clients?

Answer:

Helpful meeting adjustments may include sending an agenda in advance, limiting the number of decisions, using shorter meetings, reducing screen clutter, muting alerts, choosing a quieter room, avoiding rapid topic changes, and ending with a recap. These adjustments can help clients preserve decision energy and leave the meeting with a clearer understanding of what happens next.

Question:

How can an adviser check understanding without embarrassing the client?

Answer:

Instead of asking, “Does that make sense?” an adviser can say, “I want to make sure I explained that clearly. What do you understand the next step to be?” This frames the question as a check on the adviser’s explanation, not a test of the client. The client’s restatement helps reveal whether the recommendation, reason, timing, and action step are understood.

Question:

Why are automation and checklists useful for neurodivergent clients?

Answer:

Automation and checklists reduce reliance on memory, motivation, and repeated decision-making. Scheduled contributions, autopay, recurring reviews, direct links, prefilled forms, and short written action lists can make responsible financial behavior easier to complete. Automation should still be explained, reviewed, and controlled by the client.

Question:

What is the difference between a brake and a bridge in financial planning for neurodivergent individuals?

Answer:

A brake slows action that may be impulsive, such as a waiting period before a major trade or written confirmation before reallocating assets. A bridge helps action happen, such as a checklist, staged instructions, scheduled reminder, or same-day recap. In financial planning and ADHD, a brake may reduce impulsive decisions. In financial planning for autistic individuals, a bridge may make change feel more predictable and manageable.

Question:

Are these practices only for clients with a formal diagnosis?

Answer:

No. Many clients who benefit from these practices have no diagnosis. Some simply struggle with math, paperwork, spatial reasoning, ambiguity, sensory distractions, or follow-through. Better agendas, clearer language, written summaries, and simpler implementation steps help diagnosed clients, undiagnosed clients, and clients who only have a “touch” of these traits.

Question:

How many forms of neurodivergence are known to exist?

Answer:

There is no single official count of forms of neurodivergence. Autism and ADHD are two of the best-known examples, but the broader term is often used to include learning differences, communication differences, sensory processing differences, tic disorders, genetic developmental conditions, and other neurological or cognitive variations. The article includes a working list of commonly discussed examples.

Question:

What role did Frank Murtha play in this work?

Answer:

Frank Murtha, Ph.D., helped turn the idea into adviser education by bringing psychological insight, teaching discipline, and practical client-service framing to the subject. The collaboration matters because it translates a complex human topic into adviser behavior: better questions, clearer language, calmer meetings, stronger follow-up, and more dignity for clients.

Question:

What is the main takeaway for IA reps, CFPs, CPAs, CIMAs, and other financial professionals?

Answer:

The main takeaway is that technically correct advice is not enough. Advice must be understandable, retainable, and executable by the client in front of you. Financial planning for neurodivergent individuals improves communication, reduces implementation risk, and helps advisers serve clients with more respect and practical effectiveness.