Table of Contents

- Comments on the SEC proposal for semiannual reporting analyzed for investment fiduciaries

- Comments on SEC semiannual reporting proposal: what Form 10-S would change

- Fiduciaries and semiannual reporting: stuck in the middle with you

- Comments on semiannual reporting rule: what retail investors, advisers and investment clubs show

- Summary Findings from Comments on SEC proposal for semiannual reporting

- DOCE® self-study class design: earn CE credit by reading when the reading is engineered

- SEC proposal for semiannual reporting CE Learning Objectives

- FAQs

Comments on the SEC proposal for semiannual reporting analyzed for investment fiduciaries

Comments on the SEC proposal for semiannual reporting are overwhelmingly negative with the comment period scheduled to end July 6, 2026. The proposed rule change is about much more than a shift in filing frequency from quarterly to six months. The proposed rule would allow publicly-traded companies to elect to slash in half regularly required financial snapshots and provide less transparency into the business's financial condition than has been required for over half a century.

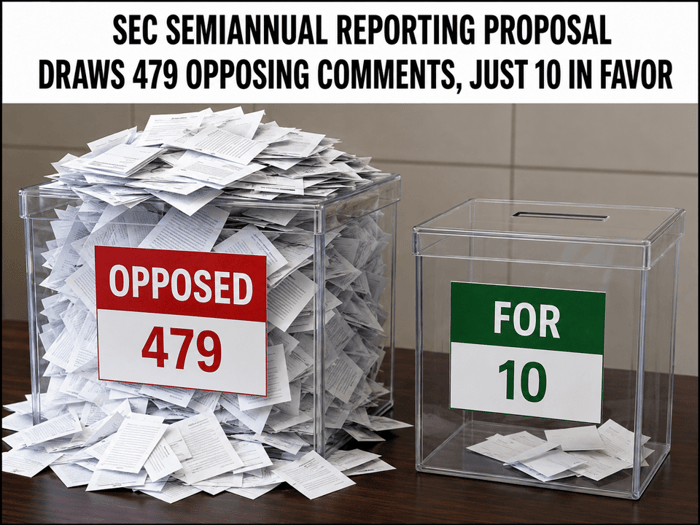

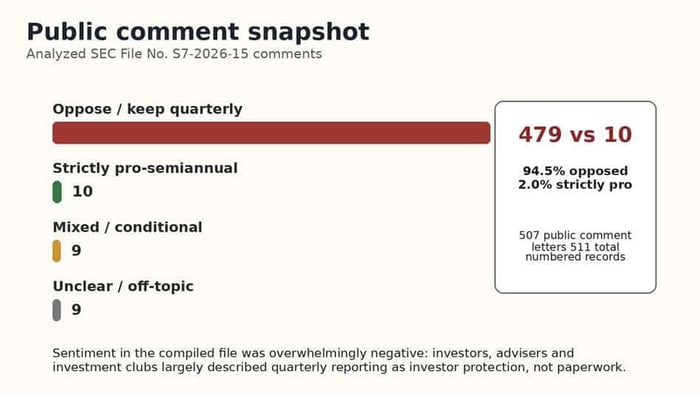

The May 30 comment compilation analyzed 511 public comments. Of that, 479 opposed the shift or urged the SEC to retain quarterly reporting, while only 10 were pro-semiannual.

Public comments first appeared on the SEC public website May 5, 2026 and the SEC says comments must be received on or before July 6, 2026. Among comments taking a clear side, the analyzed file is roughly 98% opposed and 2% in favor.

The SEC proposal for semiannual reporting would, if adopted by the Commission, permit Exchange Act reporting companies that currently file Form 10-Q to elect semiannual interim reporting using a new Form 10-S. The annual Form 10-K would remain a requirement. The Commission describes the change as optional for issuers, but investors would experience the resulting information gap whether or not they voted for it. Herein lies the rub: Semiannual financial reporting under the proposed rule would be optional for companies, but the heightened risk the rule change would create is not optional for fiduciaries. If you're searching for analysis of comments on SEC proposed rule on semiannual reporting analyzed for investment fiduciaries

Fiduciaries and semiannual reporting collide at the point where a portfolio holding no longer supplies the same regular 10-Q evidence. A fiduciary still would be required to monitor risk, explain recommendations, and document a prudent process. That process becomes much harder, however, when companies are permitted to provide financial statements only every six months.

It is hard to overstate how significant the SEC proposal for semiannual reporting would be to American accounting and public-company disclosure requirements if it adopted by the Commission. The proposal would not change Generally Accepted Accounting Procedures (GAAP), legalize aggressive accounting, or repeal anti-fraud rules. It would merely change the frequency of required disclosures of a public-company's financials, which increases uncertainty about investing in it.

The American accounting and disclosure system — GAAP, independent audits, Public Company Accounting Oversight Board (PCAOB) supervision, officer certifications, MD&A, EDGAR, XBRL, Form 8-K, Form 10-Q, and Form 10-K — is a financial marvel to the world because it makes public companies accountable to investors.

Other nations also have credible investor-protection rules and some may even be stricter in some ways than the U.S. But the American advantage has never come from any single filing requirement. It comes from an institutional system: GAAP, independent audit culture, the SEC, the PCAOB, stock exchanges, SROs, disclosure lawyers, underwriters, courts, enforcement, EDGAR, and a long habit of making public companies answer to public investors.

That structure reflects a uniquely American approach to credit and markets. From Alexander Hamilton forward, U.S. financial strength has depended on confidence that capital can move freely because institutions make promises credible. The United States does not have perfect rules. It has rules, oversight, market discipline, and institutional memory strong enough to make public investment broadly trusted. That's why the SEC proposal for semiannual reporting is so important. Other economies may protect investors well, or even better in selected ways, but none matches the scale and importance of U.S. public markets.

The issue is what happens when the world’s largest capital market reduces the required frequency of standardized public financial information. If the world sees U.S. regulation as moving toward opacity, does the world start to question their trust in US capital markets? Will investors worldwide still view the U.S. financial system as stable because markets get information that is timely, comparable, enforceable, and available to all?

Figure: Public comment snapshot - 479 opposed or keep-quarterly comments versus 10 strictly pro-semiannual comments.

Comments on SEC semiannual reporting proposal: what Form 10-S would change

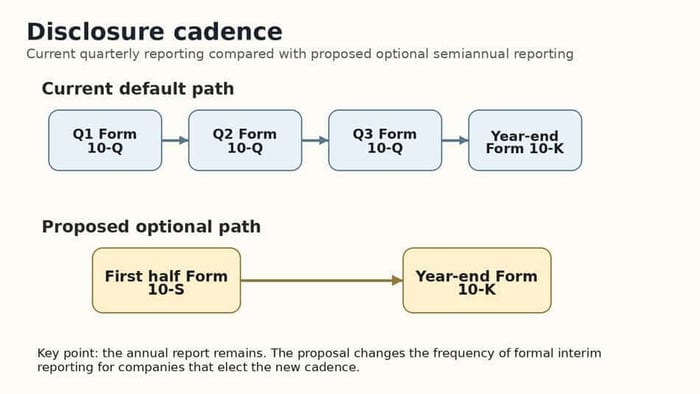

The SEC proposal for semiannual reporting would not abolish the annual report or repeal the Exchange Act. It would change the Commission's interim-reporting rules under Exchange Act Sections 13(a) and 15(d). Today, most domestic Exchange Act reporting companies file three Form 10-Q reports each fiscal year, with the fourth quarter folded into Form 10-K. The proposal would keep quarterly reporting as the default, but let eligible companies elect semiannual interim reporting by filing one new Form 10-S for the first six months of the fiscal year and one Form 10-K for the full year.

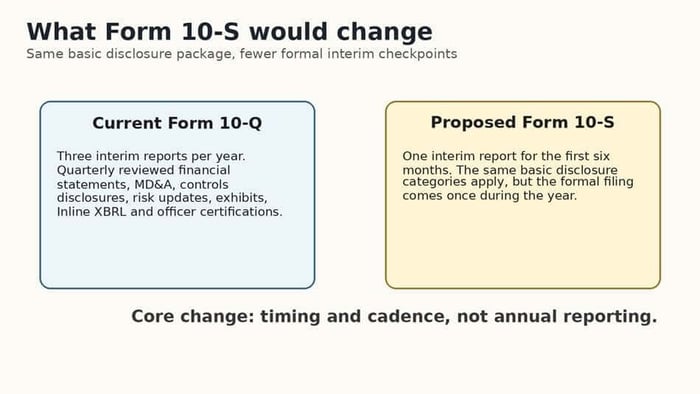

Form 10-S would not be lighter than Form 10-Q on its face; the major change is that the formal interim filing would come once, not three times, during the fiscal year.

The proposed Form 10-S would be an optional six-month interim report for electing Exchange Act reporting companies. Form 10-Q would remain the default path for companies that do not elect the new cadence, and Form 10-K would stay in place. The core change is interim timing, not annual reporting.

The proposed Form 10-S is the centerpiece. The SEC says it would require the same narrative disclosures and financial information as Form 10-Q, but it would cover a six-month period rather than three months. That means management discussion and analysis (MD&A), market-risk disclosure where applicable, disclosure controls and procedures, material changes in internal control over financial reporting, legal proceedings, risk-factor changes, unregistered sales, defaults, insider-trading-plan disclosure, exhibits, Inline Extensible Business Reporting Language (XBRL), and officer certifications would travel into the semiannual form. The SEC proposal also asks whether accounting or auditing standards would need to change if the proposal is adopted, which is why this is not merely a filing-calendar story.

The election mechanics is simple but important. A company would elect semiannual reporting by checking a new box on Form 10-K, or by checking a similar box on an initial registration statement. A company would be locked into that cadence for the fiscal year. If it leaves the box unchecked, it remains a quarterly filer. If it mistakenly checks or fails to check the box, the proposal would allow a corrective Form 10-K amendment within a limited period.

The SEC's policy argument is a tradeoff. On the issuer side, the Commission points to lower compliance cost, less management distraction, fewer auditor reviews, lower XBRL and legal costs, and possibly more companies willing to become or remain public. On the investor side, the release acknowledges costs: delayed standardized information, reduced comparability between quarterly and semiannual filers, possible increases in information asymmetry, possible reduced analyst coverage, less frequent internal-control disclosure, and possible pressure on capital-raising practices if underwriters or lenders still demand quarterly financial information.

The accounting profession's silence thus far is notable. AICPA and PCAOB, two powerful accounting institutions, have not yet commented on the SEC proposal for semiannual reporting. The uploaded comment compilation did not identify a standalone comment letter from the AICPA or a standalone comment from a current or former PCAOB board member. However, the file includes an SEC staff meeting with representatives of the North Carolina Association of Certified Public Accountants, representatives of PricewaterhouseCoopers LLP, and Representative Tim Moore. It also includes a detailed practitioner comment from Margaret Rosenfeld of Zukunft Advisory urging the Commission to coordinate with the PCAOB and AICPA on interim review work for semiannual filers.

The accounting and audit question is not only whether Form 10-S would be reviewed. It is what happens when a semiannual filer still communicates quarterly through earnings releases, calls, investor slide decks, or Form 8-K items without the same formal Form 10-Q scaffolding. Ms. Rosenfeld's comment called this a disclosure liability gap and argued that, without guidance, issuers and boards may negotiate auditor involvement case by case, compromising the integrity of the information.

Figure: Current quarterly reporting cadence compared with the proposed optional semiannual path.

Figure: Form 10-S changes the timing of formal interim reporting, not the existence of annual reporting.

Fiduciaries and semiannual reporting: stuck in the middle with you

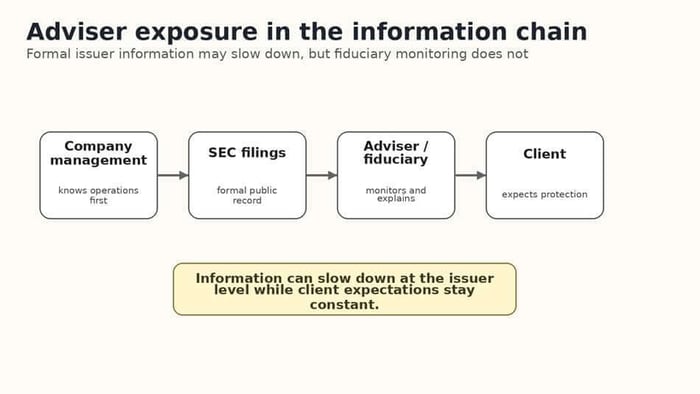

Advisers are not the company, the auditor, or the SEC. But they are the professional in front of the investor when a company disappoints. Fiduciaries should view semiannual reporting as an information-chain issue.

If a company moves from quarterly reporting to semiannual reporting, the adviser may have less formal, standardized information to review. Earnings releases, Form 8-Ks, conference calls, investor presentations, and management guidance may still continue to be provided, but they are not identical substitutes for a reviewed Form 10-Q. Some are voluntary. There are no rules standardizing conference call disclosures, for example. Press statements are furnished rather than filed and less standardized. Investor presentation don't necessarily include the same financial-statement structure, controls disclosure, MD&A depth, or officer certification framework. That raises adviser risk and liability.

Clients still expect their adviser to know when a company's fundamentals are deteriorating, even if the public filing cadence has slowed and the IAR is operating on less information. In that sense, advisers can become stuck in the middle with investors in a less transparent chain. They did not create the reporting gap, but they may be blamed if a negative trend, accounting concern, or business deterioration becomes obvious only after a six-month interval.

That does not mean every semiannual filer would become unsuitable. It means the fiduciary process should change if the SEC proposal for semiannual reporting is adopted. Advisers and committees may need to identify which holdings elect Form 10-S, evaluate substitute disclosures, compare peers, watch liquidity and analyst coverage, and document whether a holding remains appropriate. The duty is not to predict the future. The duty is to use a prudent process with the information available.

Figure: Adviser exposure in the information chain. Formal issuer information may slow down, but fiduciary monitoring does not.

Comments on semiannual reporting rule: what retail investors, advisers and investment clubs show

The public comments are useful because they show how investors actually use the existing system. Many commenters said quarterly reports help them decide whether to buy, hold, sell, trim, rebalance, or continue studying a company. The comments on semiannual reporting rule repeatedly frame quarterly reporting as the one standardized information channel available to ordinary investors who do not have management access, analyst teams, or expensive alternative data.

For this analysis, commenters are categorized as retail investors, advisers or financial professionals, and investment club members. Each group is a proxy for an investor profile that is important to understand. Retail investors represent end owners relying directly on public filings. Advisers and financial professionals represent fiduciary monitoring and client implementation. Investment club members represent grassroots investor education and collaborative stock-study discipline.

The file also has an audience story. At least 300 comments mentioned investors, at least 160 explicitly identified as retail, individual, private, personal, retirement, or self-directed investors, 42 identified with financial, accounting, investing, advisory, or capital-markets credentials, and 16 referenced investment clubs, Better Investing, NAIC, club members, or similar groups. Those club comments are valuable because they show public-company reporting as investor education.

The policy question is not whether disclosure costs money. It does. The question is whether the public-market bargain should change if the SEC proposal for semiannual reporting is adopted. Public companies receive access to public capital, liquidity, analyst attention, employee equity programs, index inclusion, and a market price. In return, many commenters argue that they owe public investors a recurring, standardized, comparable update. The comments on the SEC proposal for semiannual reporting show that ordinary investors view that update as investor protection, not paperwork.

Figure: Commenter groups as investor proxies. Different groups use quarterly reporting in different ways.

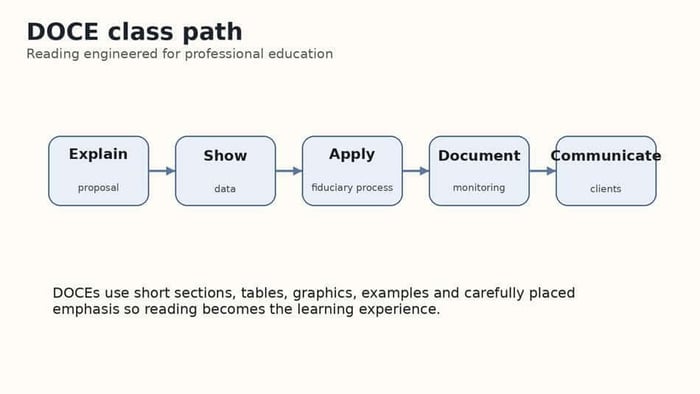

DOCE® self-study class design: earn CE credit by reading when the reading is engineered

A DOCE® is a self-study delivery style for professionals who like to learn by reading CE and CPE. It is different from a magazine article with a quiz attached. A magazine may inform, but it is not engineered expressly to help a reader achieve specific learning outcomes. DOCEs® use short sections, graphics, tables, examples, review prompts, and carefully placed emphasis so the reading itself becomes the learning experience.

The CE version provides deeper analysis with comment-file classification, fiduciary checklists, issuer arguments, market-risk issues, regulatory history, accounting-profession signals, and practical client communication tools. The DOCE® method explains, shows, applies, and helps readers retain information. It's skimmable reading. It takes about half the time as a webinar to earn one credit of CE or CPE.

Figure: DOCE® class path for this self-study reading.

SEC proposal for semiannual reporting CE Learning Objectives

By the end of this DOCE® class, the learner should be able to:

✓ Describe the SEC proposal to permit optional semiannual reporting on new Form 10-S.

✓ Distinguish Form 10-Q, Form 10-S, Form 10-K, Form 8-K, earnings releases, and earnings guidance.

✓ Explain the main themes in the comments on semiannual reporting rule.

✓ Identify how retail investors and investment clubs use quarterly reports.

✓ Analyze fiduciaries and semiannual reporting from a monitoring-process perspective.

✓ Evaluate the issuer-side arguments about compliance burden, public-company costs, and short-termism.

✓ Recognize information-asymmetry, volatility, and price-discovery risks raised by commenters.

✓ Separate quarterly historical reporting from quarterly forward-looking earnings guidance.

✓ Develop questions fiduciaries should ask if holdings move to semiannual reporting.

✓ Communicate the proposal’s practical implications to clients, committees, or audiences.

Comment-file snapshot

Data point | Count or insight |

Numbered records analyzed | 511 |

Public comment letters | 507 |

SEC meeting memoranda / meetings | 4 |

Oppose / keep quarterly | 479 public comments |

Strictly pro-semiannual | 10 public comments |

Mixed or conditional | 9 public comments |

Investment club / Better Investing / NAIC references | 16 |

Financial-professional or credentialed records | 42 |

Public comments first appeared in analyzed file | May 5, 2026 |

SEC comment deadline | July 6, 2026 |

FAQs

What are the comments on SEC proposed rule on semiannual reporting about?

The comments on SEC proposed rule on semiannual reporting focus on whether public companies should keep filing quarterly Form 10-Q reports or be allowed to elect semiannual reporting on new Form 10-S. The central issue is not just filing frequency. It is whether investors would still receive timely, standardized, comparable public-company information often enough to make informed decisions.

What would the SEC semiannual reporting proposal change?

The proposal would let eligible Exchange Act reporting companies file one semiannual Form 10-S for the first six months of the fiscal year instead of three quarterly Form 10-Q reports. Form 10-K would remain in place for the full fiscal year. Form 10-Q would remain the default for companies that do not elect semiannual reporting.

Would Form 10-S be lighter than Form 10-Q?

Not on its face. The proposed Form 10-S would generally require the same narrative disclosures and financial information as Form 10-Q, but it would cover a six-month period instead of a three-month period. The main change is timing: formal interim reporting would come once during the fiscal year, not three times.

Why do fiduciaries and semiannual reporting belong in the same discussion?

Fiduciaries and semiannual reporting belong together because fiduciaries still must monitor client holdings even if issuers provide formal public information less often. If a company stops filing quarterly Form 10-Qs, advisers, trustees, and investment committees may need to identify substitute disclosures, compare peers, document monitoring decisions, and explain the changed information environment to clients.

What do the comments on semiannual reporting rule say about retail investors?

The comments on semiannual reporting rule show that many retail investors rely on quarterly reports to monitor public companies, evaluate risks, compare performance, and make buy, hold, sell, trim, or rebalance decisions. Many commenters frame Form 10-Q as the standardized information source available to ordinary investors who do not have management access, analyst teams, or alternative data.

How many comments opposed the SEC semiannual reporting proposal?

In the analyzed comment compilation, there were 511 numbered records, including 507 public comment letters and 4 SEC meeting memoranda. Of the public comments, 479 opposed the shift or urged the SEC to keep quarterly reporting. Only 10 were counted as strictly pro-semiannual, with 9 more classified as mixed or conditional.

Why are investment club comments important?

Investment club comments matter because they show that quarterly reports are not only used by professional analysts. Investment club members described using Form 10-Qs to update stock studies, discuss buy and sell decisions, compare companies, and educate members. In that sense, investment club members are a proxy for grassroots investor education and collaborative stock-study discipline.

How are retail investors, advisers, and investment club members different in this analysis?

Retail investors represent end owners who rely directly on public filings. Advisers and financial professionals represent fiduciary monitoring, portfolio implementation, and client communication. Investment club members represent investor education and group stock analysis. Each category is a proxy for a different way quarterly reports are used in real-world investing.

What investor risks are raised in the comments on SEC proposed rule on semiannual reporting?

Commenters raise concerns about delayed standardized information, wider information gaps, reduced comparability, less analyst coverage, increased volatility, weaker price discovery, and greater advantage for investors with alternative data or management access. The SEC proposal also acknowledges tradeoffs involving delayed information, comparability, information asymmetry, and capital-raising practices.

Is quarterly reporting the same as quarterly earnings guidance?

No. Quarterly reporting provides historical financial information through a formal SEC filing. Quarterly earnings guidance is forward-looking management communication about expected results. Many commenters argue that if short-termism is the concern, regulators should address excessive earnings guidance rather than reduce standardized quarterly historical reporting.

Would Form 8-K replace Form 10-Q if companies elect Form 10-S?

Form 8-K would still require or permit disclosure of certain material events, but it is not a full substitute for quarterly Form 10-Q reporting. The attached draft notes that the proposal relies partly on Form 8-K and Regulation FD, while also acknowledging that earnings releases are not the same as reviewed Form 10-Q financial statements.

Why do some commenters support semiannual reporting?

Supporters or conditional supporters argue that quarterly reporting can impose public-company costs, management distraction, legal and accounting burdens, audit-review work, and XBRL-related costs. Some believe optional semiannual reporting could help smaller companies, emerging growth companies, or development-stage issuers focus more on long-term operations and less on quarterly reporting cycles.

Why do many commenters oppose semiannual reporting?

Many commenters oppose semiannual reporting because they view quarterly reports as part of the public-market bargain. Public companies benefit from public capital, liquidity, analyst attention, and market valuation. In return, commenters argue that public investors deserve recurring, standardized, comparable updates that help them monitor risk and hold management accountable.

What should fiduciaries ask if a company moves to semiannual reporting?

Fiduciaries should ask what information disappears, what replaces the missing Form 10-Q, whether substitute disclosures are reviewed or comparable, whether peers still report quarterly, whether the issuer is volatile or thinly covered, and what decision rule governs holding, trimming, selling, or communicating a changed monitoring process.

How can advisers explain comments on SEC proposed rule on semiannual reporting to clients?

Advisers can explain that the SEC proposal may let some companies provide formal interim financial statements less often. That does not automatically make those companies unsuitable, but it changes the monitoring process. Advisers can tell clients they will identify affected holdings, review substitute disclosures, compare peers, and document whether each holding remains appropriate.

Can clients submit comments on the SEC semiannual reporting proposal?

Yes. The draft includes a client email explaining that clients and community groups can submit comments by email to the SEC, using File Number S7-2026-15 in the subject line. It also advises clients not to include private personal information because submitted comments may be posted publicly.

What is the simplest takeaway from the comments on semiannual reporting rule?

The simplest takeaway is that disclosure cadence is market infrastructure. The comments on semiannual reporting rule show that many retail investors, advisers, and investment club members view quarterly reports as essential to transparency, accountability, investor education, and fiduciary monitoring. The pro-flexibility side focuses on issuer burden and whether some companies need quarterly reporting less than others.